What Does Homeowners Insurance Cost in Jacksonville and Northeast Florida? (2026 Real Data)

Quick Answer:

- Based on 2,000+ Jacksonville policies, most homeowners pay between $1,945 and $4,071 per year.

Median premium: $3,004

Average premium: $3,454 per year

The right price for your home depends on which carrier writes it. We compare home insurance across 26 Florida companies for Jacksonville homeowners — pricing varies $1,500 to $2,000 between carriers for the same home.

What this means for you:

Averages can be misleading. Two similar homes can vary $500-2000 a year based on:

- Roof

- Home Age

- Location

- Coverage choices

- Claims history

Takes 5 minutes. No pressure. No spam.

This data below reflects real homes across Duval, St. Johns, Clay, and Nassau counties, including areas like Jacksonville, St. Augustine, Ponte Vedra Beach, Nocatee, Orange Park, and Fleming Island.

Unlike comparison websites, what's below is not modeled estimates. These are actual premiums on real policies with strong coverage — replacement cost on the home and contents, $300,000 or higher liability on most policies, and endorsements like water backup and personal injury where appropriate.

We don't reduce coverage just to make the price look better. Our goal is simple: real protection at the best possible price.

What follows breaks down what actually drives these numbers and how you can influence what you pay. We break down:

- What’s driving these price ranges

- Why some homes cost significantly more

- What you can do to lower your premium

Who's Behind This Data

I'm Susan Augustyniak, and I've been licensed in the insurance industry since 1999. I hold the CIC (Certified Insurance Counselor) designation.

Before joining Augustyniak Insurance Group in 2008, I spent nine years at Nationwide, where I worked as a commercial underwriter, large loss property claims adjuster, and sales manager.

Over the course of my career, I've reviewed thousands of homeowners insurance policies across Duval, St. Johns, Clay, and Nassau counties. This article is based on that experience, along with real data from our agency's current book of business.

Why These Numbers Are Higher Than What You See on Comparison Websites

If you've already searched online, you've probably seen estimates in the $1,500 to $2,000 range.

Those numbers aren't wrong, but they're based on lower coverage. Most are modeled using $250,000 to $300,000 in dwelling coverage, minimal endorsements, and baseline liability limits.

Our data reflects what homeowners actually pay when their home is insured for what it would truly cost to rebuild. Across our book of business, the median dwelling coverage is over $430,000, and 93% of our clients carry $300,000 or more in liability protection.

When we isolate policies in that same lower dwelling range, our premiums average about $2,475 per year.

The difference isn't overpricing.

It's coverage.

What's Behind the Price DifferenceComparison website estimates vs. what proper coverage actually costs

Jacksonville & Northeast Florida Homeowners Insurance: 5 Key Findings From 2,000+ HO-3 Policies

After analyzing over 2,000 active homeowners policies across Jacksonville and the surrounding Northeast Florida area, five clear patterns emerged. Most homeowners are surprised by at least one of them.

Below is a quick summary. We'll break down each finding in detail and show how it impacts your premium.

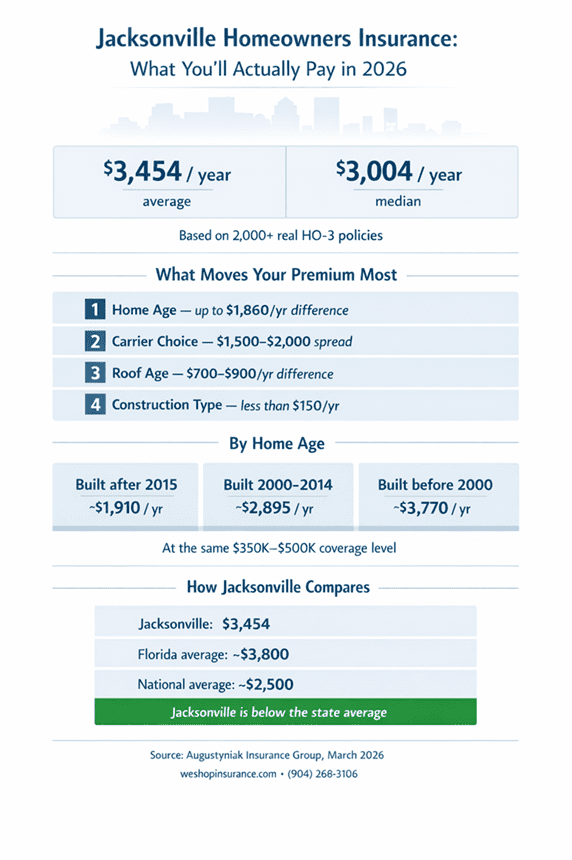

1. The average premium is $3,454 per year, but most fall in a range.

The average homeowners insurance premium in Jacksonville and Northeast Florida is $3,454 per year, with a median of $3,004.

Most homeowners with proper coverage pay between $1,945 and $4,071.

For context, Florida's statewide average is around $3,800, while the national average is about $2,500 for a home with $400,000 in dwelling coverage.

Across Northeast Florida, including areas like Jacksonville, St. Augustine, and Orange Park, home insurance is generally below the state average and significantly less expensive than South Florida.

2. Home age is the single biggest pricing factor.

At the same coverage level, a home built before 2000 averages about $3,770 per year. A home built after 2015 averages about $1,910. And a brand new home is even less. That is a gap of nearly $1,800 per year for the same amount of coverage.

3. Roof age adds approximately $700 to $900 per year.

Once a roof exceeds the 10-year mark, the aged roof factor adds between $700 to $900 a year. This is with replacement cost roof coverage. Recent Florida market changes now give homeowners with older roofs more options than they had even six months ago.

4. ZIP code matters, but less than the home itself.

The most expensive ZIP code in our data, Ponte Vedra Beach, averages over $6,500 per year, largely due to higher home values and coastal exposure.

More affordable areas like Green Cove Springs average around $2,250 per year.

However, newer communities like Nocatee often pay about 0.5% of home value annually, which is less than half the rate of many older neighborhoods across Jacksonville and surrounding areas.

5. Carrier pricing varies dramatically.

We routinely see the same home quoted $1,500 to $2,000 apart between different companies. No single carrier is the cheapest for every home.

- Now Let's Dive into the Details

What Do Most Northeast Florida Homeowners Actually Pay for Home Insurance?

For a typical Northeast Florida home, around 1,800 to 2,500 square feet with $350,000 to $500,000 in dwelling coverage, most homeowners are paying roughly $2,800 to $4,000 per year in 2026.

However, no two homes are priced the same. Your insurance rate is based on your property's risk profile, location, and coverage choices.

The chart below highlights the key factors that have the biggest impact on your premium.

From there, we'll break down each one in detail, including how home age, insurance company selection, roof age, coverage levels, ZIP code, and construction type can significantly increase or decrease what you pay.

These factors vary across Northeast Florida, including areas like Jacksonville, St. Johns County, and Clay County.

Home Age: The Biggest Factor Most People Overlook

Most homeowners assume their ZIP code or insurance company is the main reason their premium is what it is. In our data, neither is the biggest driver.

The single most important factor is when your home was built.

Distance to the coast still matters. A home near the beach will cost more than a similar home inland in areas like Clay County. But even then, home age has a greater impact on your premium than almost anything else.

To show how significant this is, we compared homes with the same coverage — between $350,000 and $500,000 in dwelling coverage — so the primary difference is the age of the home.

| Year Built | Avg. Annual Premium |

|---|---|

| After 2015 | ~$1,910 |

| 2000–2014 | ~$2,895 |

| Before 2000 | ~$3,770 |

Source: Augustyniak Insurance Group, 2,000+ active HO-3 policies, March 2026.

That's a difference of nearly $1,800 per year, or about $150 per month, for the same amount of coverage on an older home.

Over 10 years, that adds up to roughly $18,000 in additional insurance costs.

Real-Life Example: Same ZIP Code, $1,800 Apart

We insure two homes in the 32259 ZIP code, both carrying similar dwelling coverage around $450,000. One was built in 2019 with a hip roof, impact-rated garage door, and current building code construction. That homeowner pays under $2,100 per year. The other was built in 1994, frame construction, with a shingle roof installed in 2012. That homeowner pays over $3,900. Same area, similar coverage, $1,800 apart.

Newer homes are built to Florida's current building code, which requires significantly stronger wind resistance than codes from the 1980s and 1990s. They have newer roofs, updated wiring and plumbing, and modern materials that reduce the frequency and severity of claims. Carriers see the difference in their loss data and price accordingly.

If you are shopping for a home and weighing a 1998 build against a 2018 build at similar prices, insurance cost should be part of that calculation. The newer home could save you $1,500 or more per year on insurance alone.

For a look at which companies dominate the Florida market by policy count, see our list of the 25 largest homeowners insurance companies in Florida.

Roof Age: The Factor That Can Lock You In or Open Up Options

After home age, the condition and age of your roof is the next biggest cost driver. Florida insurers place heavy weight on roofs because they are your home's first line of defense against wind and water damage.

| Roof Age | Avg. Annual Premium |

|---|---|

| 0–5 years | ~$3,340 |

| 6–10 years | ~$3,675 |

| 11–15 years | ~$3,830 |

| 16–20 years | ~$4,130 |

| 21+ years | ~$3,670 |

The 21+ year group includes some homes with very high dwelling values where premium is driven more by coverage amount than roof age. The pattern is clearest at controlled dwelling levels. Source: Augustyniak Insurance Group, March 2026.

The premium difference between a newer roof and one past 10 years is roughly $700 to $900 per year at the same coverage level.

The Florida Roof Insurance Landscape Has Changed

Until late 2025, many carriers would not insure homes with roofs older than 15 years, and some drew the line at 10. If your roof was past that threshold, your only real option was to replace it before you could get acceptable coverage. Many homeowners felt stuck.

That has started to change.

Over the past six months, several carriers have begun offering coverage on older roofs with a tradeoff. Instead of full replacement cost coverage, these policies may include a roof schedule or actual cash value (ACV) settlement on the roof.

This means that if you file a claim, the insurer factors in depreciation based on the roof's age, rather than paying the full cost to replace it.

What This Means for Homeowners

This shift is significant. It gives homeowners with older roofs more options and more negotiating power than they had even a year ago.

However, it comes with tradeoffs.

ACV roof coverage typically results in a lower claim payout compared to replacement cost coverage. But for a homeowner with a 14-year-old roof who was previously told they needed to spend $15,000 to $25,000 on a new roof just to get insured, this flexibility can be a meaningful alternative.

Our advice:

If your roof is approaching 10 to 15 years old, it's worth evaluating both paths:

- Replacing the roof may lower your premium and restore access to full replacement cost coverage

- An ACV policy may provide a temporary, more affordable option until you're ready to reroof

Every situation is different, and the right decision depends on your home, your budget, and your long-term plans.

For more on how roof condition and other systems affect insurability, see our guide on 4-point inspections in Florida.

What You Pay by Coverage Level

Your dwelling coverage is the estimated cost to rebuild your home from the ground up at today's construction prices.

It is not your market value or tax-assessed value. It reflects what a contractor would charge to reconstruct your home using similar materials, current labor rates, and today's building codes.

For a full breakdown of how coverage works, see our Beginner's Guide to Homeowners Insurance in Florida.

In Northeast Florida, rebuild costs regularly exceed $200 per square foot, especially in areas like Mandarin, San Marco, and the Beaches.

That means a typical 2,000 square foot home can easily require $400,000 or more in dwelling coverage.

Across our book of business:

- The median dwelling coverage is $433,000

- More than half of policies fall between $350,000 and $600,000

For more guidance, see our article: How Much Home Insurance Do I Need in Florida?

| Dwelling Coverage | Avg. Annual Premium |

|---|---|

| Under $250,000 | ~$2,290 |

| $250,000–$350,000 | ~$2,675 |

| $350,000–$450,000 | ~$3,125 |

| $450,000–$600,000 | ~$3,575 |

| $600,000–$800,000 | ~$4,070 |

| Above $800,000 | ~$6,120 |

Source: Augustyniak Insurance Group, March 2026.

As coverage increases, premiums rise in a predictable way. But the bigger risk is not overinsuring your home. It is being underinsured.

If your dwelling coverage is significantly below $300,000 and your home is 2,000 square feet or larger, it is worth having your agent run a current replacement cost estimate.

We see homeowners every week whose coverage has not kept up with what it would actually take to rebuild.

The goal is not to insure your home for what it would sell for. It is to insure it for what it would cost to rebuild after a loss.

Insurance Cost by ZIP Code and How It Compares to Your Home's Value

In many cases, the type and age of the home matter more than the ZIP code itself. When you compare insurance cost to home value, a clearer pattern emerges.

Newer, planned communities tend to have the lowest cost relative to value.

- Nocatee (32081): Median home value around $677,000 · Average insurance: ~$3,292 · Insurance-to-value ratio: 0.5%

- Palencia (32095): Similar profile with low ratios due to newer construction and strong wind mitigation

These areas benefit from newer homes, current building codes, and better overall risk profiles.

Older, established neighborhoods often pay more relative to home value.

- San Marco (32207): Median home value around $277,000 · Average insurance: ~$3,018 · Insurance-to-value ratio: 1.1%

The homes may cost less to buy, but insurance takes a larger percentage because the housing stock is older.

Real-Life Example: Higher Home Value, Lower Insurance

We had a client move from a 1985 home in the 32225 ZIP code to a 2021 home in Nocatee. Their home value went up by nearly $200,000 but their annual insurance premium dropped by over $1,400. The newer construction, current roof, and updated building code made all the difference.

| ZIP Code | Area | Avg. Premium | Insurance-to-Value Ratio |

|---|---|---|---|

| 32082 | Ponte Vedra Beach | ~$6,550 | 0.7% |

| 32250 | Jacksonville Beach | ~$4,400 | 0.7% |

| 32224 | Atlantic / Kernan | ~$4,200 | 0.9% |

| 32223 | Mandarin South | ~$3,770 | 0.9% |

| 32259 | Julington Creek | ~$3,510 | 0.6% |

| 32081 | Nocatee | ~$3,290 | 0.5% |

| 32258 | Baymeadows | ~$2,970 | 0.8% |

| 32207 | San Marco | ~$3,020 | 1.1% |

| 32003 | Fleming Island | ~$3,070 | 0.7% |

| 32095 | Palencia | ~$2,910 | 0.5% |

| 32244 | Argyle / Westside | ~$2,680 | 1.0% |

| 32218 | North Jacksonville | ~$2,330 | — |

| 32043 | Green Cove Springs | ~$2,250 | — |

Note: 32082 includes Ponte Vedra Beach, Palm Valley, and Sawgrass. Oceanfront homes may exceed $1M in dwelling coverage, while inland homes are more moderate. Insurance-to-value ratios are based on Zillow and Redfin median home values (2026).

Premium data: Augustyniak Insurance Group, April 2026.

If you are buying a home and want to estimate insurance costs, the insurance-to-value ratio is a useful starting point. Newer communities typically run 0.5% to 0.7% of home value per year. Established neighborhoods with older housing stock often run 0.9% to 1.2%.

What This Means for You

If you're estimating insurance costs when buying a home, looking at price alone can be misleading.

A better starting point is the insurance-to-value ratio:

- Newer communities: typically 0.5% to 0.7% of home value

- Older neighborhoods: often 0.9% to 1.2% of home value

In many cases, a more expensive home can actually cost less to insure relative to its value if it's newer and built to current standards.

Want a Personalized Estimate?

If you want to know what your specific home would cost to insure in your ZIP code, the best approach is to run a real quote based on your home's details, not just averages. We would love to help.

Want Your Personalized Estimate?

County by County

We write homeowners policies across all four Northeast Florida counties. Premium differences between them are meaningful, but they are driven more by home age, construction, and dwelling value than by county alone.

| County | Avg. Premium | Median Premium |

|---|---|---|

| Clay County | ~$2,875 | ~$2,510 |

| Nassau County | ~$3,120 | ~$2,965 |

| Duval County | ~$3,430 | ~$2,955 |

| St. Johns County | ~$4,105 | ~$3,595 |

Clay County is the most affordable of the four, with typical premiums about $550 lower than Duval County and more than $1,200 lower than St. Johns County.

St. Johns County has the highest average premiums, largely due to higher home values and coastal exposure in areas like Ponte Vedra Beach.

Duval County shows the widest range. It includes everything from older Westside neighborhoods to newer Southside communities, which is reflected in the spread between its average and median premiums.

Nassau County falls in the middle, with a mix of coastal and inland homes contributing to more moderate pricing overall.

What This Means for You

Where you live matters, but what you live in matters more.

A newer home in Duval County may cost less to insure than an older home in Clay County. The county sets the stage, but your home's age, roof, and construction ultimately drive your premium.

Home Size and the Cost-Per-Square-Foot Gap

Larger homes cost more to insure because they cost more to rebuild. But size alone does not tell the full story.

| Home Size | Avg. Annual Premium |

|---|---|

| Under 1,500 sq ft | ~$2,615 |

| 1,500–2,000 sq ft | ~$2,705 |

| 2,000–2,500 sq ft | ~$3,170 |

| 2,500–3,000 sq ft | ~$3,640 |

| 3,000–4,000 sq ft | ~$4,260 |

| Over 4,000 sq ft | ~$4,625 |

The more telling pattern emerges when you factor in home age.

A 2,500 square foot home built in 1995 often pays roughly the same premium as a 4,000 square foot home built in 2020.

In other words, older homes can cost twice as much per square foot to insure as newer ones.

If your premium feels high relative to your home's size, the age of the home is likely the biggest reason.

Construction Type: Real but Modest

Frame, masonry veneer, or concrete block — many homeowners assume this is a major pricing factor.

It is not.

When we compared homes of similar age and coverage, the difference between frame and masonry construction was typically less than $150 per year.

Construction type does play a role, but it is a smaller one.

Home age, roof age, and carrier selection have a far greater impact on what you pay than what your walls are made of.

Why Comparing Carriers Matters More Than Almost Anything Else

We work with over 26 homeowners insurance carriers across Northeast Florida. One of the most consistent patterns we see is how dramatically different companies price the exact same home.

It's not unusual for the same property to be quoted $1,500 to $2,000 apart between carriers.

A home one company prices at $3,800 might come in at $2,400 with another, not because the coverage is worse, but because each carrier evaluates risk differently.

When we analyzed a group of similar homes built between 1990 and 2005 with $300,000 to $500,000 in dwelling coverage, the gap between the highest and lowest priced carriers averaged over $2,000 per year.

Real-Life Example: $1,300 Savings, Same Coverage

A homeowner came to us after their renewal increased to more than $4,200.

We reshopped the policy and placed it at $2,900 with comparable coverage. Same dwelling limit. Same deductible structure. Similar endorsements.

That's a savings of over $1,300 per year.

The difference wasn't the home.

It was the carrier.

Why This Happens

Insurance pricing isn't static.

Carriers constantly adjust:

- Which ZIP codes they want to write

- How they price older roofs

- How heavily they weigh claims history and construction

A company that was competitive last year may not be competitive today.

What This Means for You

If you're only getting one quote, you're not really seeing the market.

The only way to know where your home truly falls is to compare across multiple carriers, using the same coverage structure.

That's where working with an independent agency makes a difference.

For a look at which companies are most active in Florida right now, see our Top 25 Florida Homeowners Insurance Companies ranking.

This happens constantly. Markets shift, companies change their appetite for certain ZIP codes or roof ages, and the Florida home insurance market continues to evolve.

Want to see what your home would cost across 26+ carriers?

Get a Real Quote based on Your Home, Not an Estimate or call (904) 268-3106

Are You Actually Covered?

If your first reaction to a $3,454 average premium is "that seems high," you're not wrong to question it.

But the real question isn't whether the number is high or low.

It's whether the coverage behind that number would actually protect you after a major loss.

Why Are National Websites Showing Lower Average Costs?

The $1,500 to $2,000 estimates you see online usually reflect three things:

Lower coverage. Fewer protections. More risk.

1. Lower dwelling coverage

Most comparison sites model homes at $200,000 to $300,000 in coverage.

In Northeast Florida, rebuild costs now exceed $200 per square foot.

A 2,000 square foot home modeled at $250,000 could be underinsured by $150,000 or more and that gap comes out of your pocket after a claim.

2. Minimum endorsements and low liability

A $100,000 liability limit and no additional endorsements can save a few hundred dollars per year.

But if someone is injured on your property and sues for $400,000, that savings disappears instantly.

3. Lowest-cost carrier regardless of stability

A lower premium doesn't help if the carrier:

- Delays claims

- Underpays losses

- Or becomes insolvent

Florida has seen multiple insurers go out of business in recent years, leaving homeowners scrambling to find coverage.

Our policies are built differently.

Nearly every policy in our data is an HO-3 with replacement cost on the home and contents and $300,000 or higher liability (93% of our book).

Most include endorsements like water and sewer backup and personal injury protection. Some even carry extended replacement cost.

These are not stripped down policies.

If you want confidence that your coverage will hold up after a loss, see our Jacksonville home insurance guide with full coverage details and 26-company comparison.

How to Lower Your Florida Home Insurance Premium

Based on what we see across more than 2,000 policies, these strategies make the biggest real-world difference:

Get a wind mitigation inspection

Florida insurers are required to offer discounts for verified wind-resistant features. Savings of $500 to $1,000+ per year are common.

Keep your roof current or explore the new ACV options

Homes with newer roofs often pay $700 to $900 less per year. New ACV roof options may provide flexibility for older roofs.

Compare carriers

Pricing can vary $1,500 to $2,000 between companies for the same home. A quick review can uncover meaningful savings.

Review your deductible

Increasing your deductible from $1,000 to $2,500 or even $5,000 can lower your premium. Just be sure you're comfortable with the higher out-of-pocket cost.

Bundle thoughtfully

Bundling home and auto can help, but never trade strong coverage for a small discount.

Bottom line:

Most Northeast Florida homeowners pay between $2,800 and $4,000 per year, but your home's age, roof, and coverage matter far more than the average.

Frequently Asked Questions About Homeowners Insurance Costs

How much does homeowners insurance cost in Jacksonville in 2026?

Based on our analysis of over 2,000 active policies, $3,454 per year on average with a median of $3,004. Most homeowners pay between $1,945 and $4,071. Newer homes built after 2015 typically cost around $1,900 at similar coverage levels. Homes built before 2000 average approximately $3,750. For context, Florida's statewide average is approximately $3,800, meaning Jacksonville runs slightly below the state average.

Why is my premium so much higher than what I see on comparison websites?

Most comparison sites model quotes using $200,000 to $300,000 in dwelling coverage with minimum endorsements. Our data reflects replacement cost HO-3 policies with a median dwelling coverage over $430,000, with 93% carrying $300,000 or more in liability. Many of these policies include endorsements like water and sewer backup and personal injury protection. Lower modeled coverage produces lower numbers but also produces policies that would leave most homeowners significantly short after a real loss.

How much can I save with a newer roof?

In our data, homes with roofs less than 5 years old pay approximately $700 to $900 less per year than homes with roofs over 10 years old at the same coverage level. A new roof also opens access to more carriers and better coverage terms.

Can I get insured with a roof over 15 years old?

Yes, and your options have recently expanded. Until late 2025, most Florida carriers refused older roofs entirely. Over the past six months, several carriers have begun offering policies with actual cash value or roof schedule provisions. Your payout on a roof claim accounts for depreciation, but it gives homeowners previously shut out of the market real alternatives.

How much does homeowners insurance vary between carriers for the same home?

We routinely see $1,500 to $2,000 in premium difference between carriers for the identical home, coverage level, and deductible. Each company uses different models to weigh risk factors. In some cases, the gap between the most and least expensive carrier for the same home exceeds $2,000.

What is the cheapest ZIP code for homeowners insurance in Jacksonville?

In our data, Green Cove Springs (32043) averages approximately $2,250 per year and North Jacksonville (32218) averages approximately $2,330. The most expensive is Ponte Vedra Beach (32082) at over $6,500.

How does home age affect my premium?

It is the single biggest factor. At the same coverage level ($350,000 to $500,000), homes built after 2015 average about $1,910 per year while homes built before 2000 average approximately $3,770. That is a gap of nearly $1,800 per year.

What is the insurance-to-value ratio and why does it matter?

It is your annual insurance premium as a percentage of your home's market value. Newer communities like Nocatee run about 0.5%, meaning you pay roughly $5 per year for every $1,000 of home value. Older neighborhoods like San Marco run about 1.1%, more than double. This ratio helps homebuyers estimate insurance costs before purchasing.

How does Jacksonville compare to the rest of Florida?

Jacksonville's average of $3,454 is below the statewide average of roughly $3,800, and significantly lower than South Florida and coastal areas. The national average is about $2,500 for $400,000 in dwelling coverage. Florida ranks among the three most expensive states for homeowners insurance due to hurricane risk, litigation costs, and high rebuilding costs.

More Jacksonville Homeowners Insurance Guides

About This Data

This analysis is based on more than 2,000 active HO-3 homeowners insurance policies written by Augustyniak Insurance Group as of March 2026.

The data is concentrated across Northeast Florida, including Duval, St. Johns, Clay, and Nassau counties.

The typical home in this dataset:

- 1,800 to 2,800 square feet

- $350,000 to $600,000 in dwelling coverage

Policies included in this analysis:

- Replacement cost coverage on the home and contents

- $300,000 or higher liability on 93% of policies

- Common endorsements such as water and sewer backup and personal injury

All premiums reflect total annual cost, including applicable fees.

Insurance-to-value ratios are calculated using median home values from Zillow and Redfin (2026).

State and national comparison data is sourced from the Florida Office of Insurance Regulation and NerdWallet using data from Quadrant Information Services.

We update this analysis periodically to reflect changes in the Florida insurance market.

About the Author

Susan Augustyniak is a Certified Insurance Counselor (CIC) and has been a licensed Florida insurance professional since 1999.

Before joining Augustyniak Insurance Group in 2008, she spent nine years at Nationwide Insurance, where she worked as a commercial underwriter, large loss property claims adjuster, and sales manager.

She holds a Florida 2-20 General Lines Agent license and specializes in helping homeowners across Northeast Florida navigate coverage decisions, carrier selection, and claims.

Her work focuses on clients in Duval, St. Johns, Clay, and Nassau counties.

Sources

- Policy data: Augustyniak Insurance Group active book of business, March 2026 (2,000+ HO-3 policies)

- Insurance-to-value ratios: Calculated using Zillow Home Value Index and Redfin median home values (2026)

- Florida average premium: Florida Office of Insurance Regulation (2025)

- National average premium: NerdWallet using data from Quadrant Information Services (November 2025)

- Industry research: Insurance Information Institute

Discussion

There are no comments yet.