Flood Insurance

We’ll shop and help you save on your Florida Flood insurance.

Flood Insurance

Last updated:

Augustyniak Insurance Group is an independent flood insurance agency in Jacksonville, FL. We compare NFIP (National Flood Insurance Program) and private flood insurance from 10+ carriers to find the right coverage at the best price for your home.

Standard homeowners insurance does not cover flood damage in Florida. Flood insurance is usually a separate policy.

Want to skip ahead? Get your free flood insurance quote or call (904) 268-3106.

How Much Does Flood Insurance Cost in Jacksonville?

| Policy Type | Low | Typical Range | High |

|---|---|---|---|

| NFIP / Write Your Own | ~$400 | $700 – $1,200 | $5,000+ |

| Private Flood | ~$300 | $500 – $1,100 | $4,400+ |

What affects your flood insurance rate? Based on Augustyniak Insurance Group's analysis of over 500 active flood policies, these are the factors that drive the biggest premium differences:

- Flood zone designation. Properties in high-risk zones (A, AE, VE) pay significantly more than Zone X properties. But Zone X is not free. We see Zone X policies ranging from $300 to over $1,000 depending on the property.

- Distance to water. Under Risk Rating 2.0, FEMA (the Federal Emergency Management Agency) measures your property's distance to the St. Johns River, the coast, creeks, and other water sources. Closer means higher premium.

- Property elevation. Lower elevation relative to expected flood levels increases your rate. This is where an elevation certificate can sometimes help.

- Coverage amount. Higher dwelling and contents limits cost more. NFIP caps at $250,000 dwelling. Private carriers can go to $500,000 or higher.

- Foundation type. Slab, crawlspace, elevated, and basement foundations are rated differently. Elevated homes generally pay less.

- NFIP vs. private carrier. Across our book, private flood policies carry a median premium about 9% lower than NFIP. For some properties the gap is larger. For others, NFIP is the better deal.

FEMA's Risk Rating 2.0, implemented in 2021, replaced the old zone-based pricing with property-specific risk scores. Some Jacksonville homeowners saw increases. Others saw decreases. The only way to know is to quote both NFIP and private for your address.

Lowered our flood insurance. Knowledgeable and fantastic to work with.

Lillian Parnell · Google Review, March 2026

Augustyniak was a great find 5 years ago... very thorough, super easy to work with... and put money back in my pocket (even after the flood)! To compare both rates and service... you'll be glad you did.

TK Davis · Google Review, February 2026

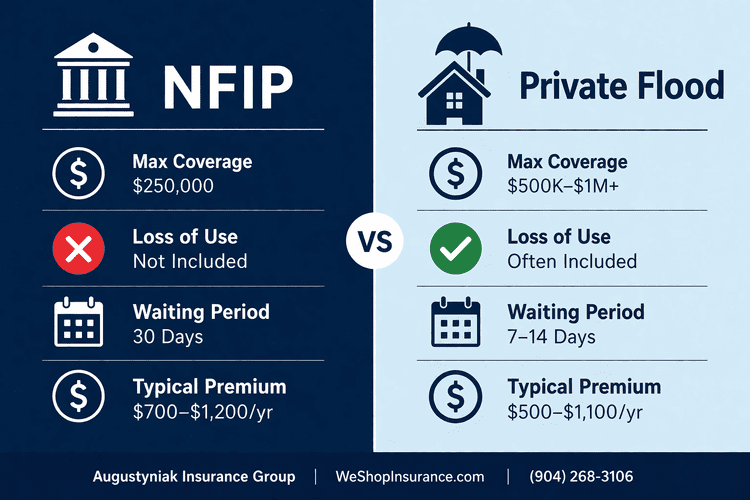

What Is the Difference Between NFIP and Private Flood Insurance?

Most people only know about NFIP because that's what their mortgage company told them to get. Makes sense.

But here's what most homeowners don't realize: Florida has a growing private flood market, and in many cases, private carriers offer more coverage for less money. We sell both. Here's how they stack up.

NFIP (National Flood Insurance Program)

- Administered by FEMA. Sold through Write Your Own carriers including Wright National, ASI Flood, Auto-Owners, and Olympus.

- Max dwelling coverage: $250,000. Max contents: $100,000.

- No loss of use coverage. If your home is uninhabitable after a flood, NFIP does not pay for temporary housing. You cover hotel stays and rentals out of pocket.

- 30-day waiting period for new policies. Waived for home purchases.

- Pricing set by FEMA under Risk Rating 2.0. Same rate no matter which WYO carrier you use.

- Monthly payment plans now available. 12 installments, no additional fee.

Now here's where it gets interesting.

Private Flood Insurance

- Our private flood carriers: Tower Hill, Beyond Flood, Flow Flood, Neptune Flood, and Titan Flood.

- Dwelling coverage above $250,000 available. Contents limits above $100,000.

- Loss of use coverage often included. If flooding forces you out of your home, many private policies help cover hotel stays, temporary rentals, and additional living expenses. This alone is one of the biggest reasons homeowners choose private over NFIP.

- Shorter waiting periods. Often 7 to 14 days instead of 30.

- Pricing varies by carrier and property. Can serve as your primary policy or as excess on top of NFIP.

How Do NFIP and Private Flood Insurance Compare?

Here's how the two options stack up across the factors that matter most to Jacksonville homeowners.

| Feature | NFIP | Private Flood |

|---|---|---|

| Backed by | FEMA (federal government) | Private insurance companies |

| Max dwelling | $250,000 | $500K to $1M+ |

| Max contents | $100,000 | Higher limits available |

| Loss of use | Not included | Often included |

| Waiting period | 30 days | Often 7–14 days |

| Payment options | Annual or 12 monthly (no fee) | Varies by carrier |

| Jacksonville CRS discount | Yes (Class 6: 10–20%) | No |

| Typical premium* | $700 – $1,200/yr | $500 – $1,100/yr |

*Based on Augustyniak Insurance Group's analysis of over 500 active flood insurance policies across Northeast Florida. Updated April 2026.

What Does Flood Insurance Cover in Florida?

Flood insurance covers damage caused by rising water from outside your home. That includes storm surge, overflowing rivers, heavy rainfall runoff, and coastal flooding.

Covered: your home's structure, foundation, electrical and plumbing systems, HVAC, built-in appliances, permanent flooring, and personal belongings like furniture, clothing, and electronics.

Not covered: landscaping, fences, pools, decks, vehicles, cash, and precious metals. And under NFIP, temporary housing is not covered. That's one reason many homeowners choose private flood instead. For broader liability protection beyond your home and auto policies, ask us about umbrella insurance.

Which Flood Insurance Carriers Does Augustyniak Insurance Offer?

We are appointed with both NFIP Write Your Own carriers and private flood markets. That means we can quote both programs for your property and show you exactly where you get the best combination of coverage and price.

NFIP / Write Your Own Carriers

These carriers sell federally backed NFIP flood policies. FEMA sets the rate, so the premium is the same regardless of which WYO carrier issues your policy. The difference is in service, claims handling, and payment options.

What Private Flood Insurance Companies Write in Florida?

Florida has one of the most active private flood insurance markets in the country. Several carriers now compete directly with NFIP, often offering broader coverage, higher limits, and competitive pricing. Here are the private flood companies we represent and what makes each one different.

- Tower Hill Insurance. Best for Florida homeowners who want a domestic carrier with local claims handling. A Florida-based company with decades of experience in the state's property and flood market. Strong option for primary residence flood coverage.

- Beyond Flood. Best for fast closings and homes above $250,000 in rebuild cost. Specializes in quick policy issuance with dwelling limits above NFIP's cap. Loss of use coverage is available.

- Flow Flood. Best for lowest premium. A competitive private flood option that frequently comes in as the lowest-cost carrier in our side-by-side comparisons. Writes residential flood across Florida in all zones.

- Neptune Flood. Best for excess flood coverage and digital-first service. A tech-forward carrier with fast online quoting. Offers both primary flood and excess flood (additional limits on top of an existing NFIP policy). Available for residential and commercial properties.

- Titan Flood. Best for properties that don't fit standard NFIP pricing. A private carrier with flexible underwriting for homes with unique risk profiles where Risk Rating 2.0 may have pushed NFIP rates higher than expected.

Not every private carrier is the right fit for every property. Rates vary significantly between carriers based on your flood zone, elevation, and distance to water. Across Augustyniak Insurance Group's active book, private flood policies carry a median premium about 9% lower than NFIP, but for some properties NFIP is still the better deal. The only way to know is to compare both.

We work with homeowners across the region. Mandarin, San Marco, Riverside, the Beaches, Arlington, Orange Park, Ponte Vedra, St. Augustine.

Every one of these areas has flood exposure. The St. Johns River and the Intracoastal don't stop at neighborhood lines. If you already have homeowners insurance, check whether it includes flood coverage. It doesn't. No homeowners policy in Florida does.

Hurricane Matthew in 2016 proved that when it pushed record storm surge up the St. Johns. If your home has never flooded, that doesn't mean it won't.

Do Jacksonville Businesses Need Flood Insurance?

Commercial properties face the same flood exposure as homes. NFIP commercial limits are $500,000 for building and $500,000 for contents. Private commercial flood options offer higher limits for larger operations.

We help Jacksonville business owners evaluate their flood exposure and find the right coverage.

Learn more: Business Insurance | Commercial Property Insurance

How Do You Get a Flood Insurance Quote in Jacksonville?

We Review

Tell us your address and current flood policy (if any). We pull your flood zone, check CRS discount eligibility, and review your coverage.

We Compare

We run your property through NFIP and private carriers side by side. Coverage, premiums, waiting periods, loss of use options.

You Choose

We present your best options with a clear recommendation. You pick the one that fits. No pressure, no games.

Ready to compare flood insurance options?

Augustyniak Insurance Group has been protecting Jacksonville homeowners since 2005. With 10+ flood carriers across NFIP and private markets, 2,250+ five-star reviews, and 12 consecutive years as a Three Best Rated agency, we find your best flood insurance option.

Monday through Friday, 8:30 AM to 5:00 PMFrequently Asked Questions About Flood Insurance in Jacksonville

Is flood insurance required in Florida?

Florida law does not require flood insurance. But if your home is in a high-risk flood zone (A, AE, or VE) and you have a federally backed mortgage, your lender will require it. Even in Zone X, we recommend it. Over 25% of flood claims nationally come from properties outside of high-risk zones.

How much does flood insurance cost in Jacksonville, FL?

Based on Augustyniak Insurance Group's analysis of over 500 active policies, the median flood premium in Jacksonville is $983 per year. Most homeowners pay between $700 and $1,200. Your rate depends on flood zone, property elevation, distance to water, and whether you choose NFIP or private coverage.

What is the difference between NFIP and private flood insurance?

NFIP is the federal flood program. Max dwelling coverage is $250,000 with no loss of use. Private flood from carriers like Tower Hill, Beyond Flood, Flow Flood, Neptune, and Titan often offers higher limits, loss of use coverage, and shorter waiting periods. We sell and compare both for every client.

Does my homeowners insurance cover flooding?

No. Homeowners insurance in Florida never covers flood damage. This is true regardless of your flood zone, your carrier, or your coverage amount. Flood insurance is always a separate policy through NFIP or a private carrier.

What flood zone is my Jacksonville home in?

FEMA assigns flood zones to every property. Zone X is lower risk. Zone A/AE is high risk. Zone VE is coastal high risk with storm surge exposure, common along Jacksonville Beach, Atlantic Beach, and Ponte Vedra. Jacksonville is a CRS Class 6 community, which gives NFIP policyholders a 20% premium discount in high-risk zones and 10% outside. Check your zone at floodsmart.gov.

Does flood insurance cover storm surge from hurricanes?

Yes. Storm surge is classified as flooding. Only a flood policy covers it. Your homeowners policy covers wind damage but not rising water. After Hurricane Matthew in 2016, many Jacksonville homeowners without flood insurance learned this the hard way. Read more: Wind vs. Flood Damage After a Hurricane.

Is there a waiting period for flood insurance?

NFIP has a 30-day waiting period from purchase date. Private flood carriers often have shorter waiting periods of 7 to 14 days. If you're buying or refinancing and your lender requires flood insurance, the waiting period is waived. Florida's hurricane season runs June 1 through November 30. Buy before you need it.

Do I need an elevation certificate for flood insurance?

Under Risk Rating 2.0, FEMA uses its own elevation data, so an elevation certificate may have less impact than before. It can still help if FEMA's data is inaccurate for your property. If you have one, send it with your quote request. If not, we can help you decide if getting one (typically $250 to $500) is worth the cost. Read more: What Is a Flood Insurance Elevation Certificate?

Susan Augustyniak, CIC

Vice President, Augustyniak Insurance Group

Certified Insurance Counselor with 25+ years in the industry. Susan has led the Augustyniak Insurance team in Jacksonville since 2005, helping thousands of Florida homeowners navigate flood insurance decisions across NFIP and private markets.

Get a

Get a