Vacant Property Insurance for Florida Real Estate Investors

When you own investment real estate in Florida, there will be periods when a property sits empty — between tenants, during a flip, while waiting for a closing, or after an inheritance.

Many investors assume their standard landlord policy or homeowners insurance will cover them during those gaps. In most cases, it won't.

In Florida, vacant investment properties are insured using a DP-1 (Dwelling Property 1) policy, also called a dwelling fire form. It's a named-peril policy designed specifically for homes that aren't occupied — and it works differently from the coverage you carry when tenants are in place.

This article is written for Florida real estate investors — landlords, flippers, and property owners managing vacant units. It supports our main guide on vacant home insurance in Florida, which covers the topic from a broader homeowner perspective.

Key Takeaway for Investors

A DP-1 dwelling fire policy is the standard way to insure a vacant investment property in Florida. It covers named perils — fire, windstorm, lightning, smoke, and explosion — but excludes accidental water damage, gradual deterioration, and theft of personal property.

Most Florida insurers classify a property as vacant after 30 to 60 days without an occupant. Once that threshold is reached, a standard landlord or homeowners policy may deny claims entirely. Investors should move their property to a DP-1 policy before the vacancy period begins.

Why Do Florida Investors Need a Vacant Home Policy?

Vacant homes carry a higher risk profile than occupied ones. Without someone present, small problems — a roof leak, a break-in, a downed tree — can go undetected for days or weeks.

Florida insurers factor this into their underwriting, which is why extended vacancy automatically triggers restrictions, exclusions, or outright claim denials on standard policies.

A DP-1 vacant home policy fills the coverage gap by providing protection for the types of losses most likely to occur when a property is empty. Common investor situations where this coverage is needed:

- Tenant turnover — the gap between one lease ending and the next beginning

- Fix-and-flip renovations — when contractors are on site but no one is living there

- Probate or estate proceedings — inherited properties that take months to resolve

- Pre-sale vacancy — a home listed for sale with no occupant

- Closing delays — a property under contract but not yet transferred

- Permit or contractor wait times — common in Florida after storm seasons

- Storm repair holdups — waiting on materials, adjusters, or restoration crews

For a broader overview — including scenarios for primary homeowners, not just investors — see our complete guide to vacant home insurance in Florida.

For owner-occupied policies, see our ranked list of Florida's largest home insurance companies.

Not sure if your property qualifies as vacant? Call us at 904-268-3106 — our team works with investors across Florida and can review your situation in minutes.

When Is Your Florida Investment Property Considered Vacant?

Most insurance companies classify a home as vacant if it has been unoccupied for more than 30 to 60 days. The exact threshold varies by carrier, but the consequences are the same: once the property exceeds the allowed vacancy period, your standard policy may deny losses that occur afterward.

For investors, vacancy happens more often than you might expect. A tenant moves out on the first of the month, you spend two weeks turning the unit, then it takes another month to find a qualified renter. You're already at 45 days — well past many carriers' thresholds.

A fix-and-flip project that was supposed to take 60 days stretches to 90 because of permit delays. A probate home sits empty for six months while the estate is settled. These gaps add up fast.

Investor Alert: New Florida Policy Language Can Void All Coverage

Many Florida carriers have updated their policy language so that all coverage is excluded — not just water and vandalism — if you fail to notify them of an occupancy change.

Under this newer language, a fire, hurricane, or liability claim can be denied entirely if the home was vacant and you didn't report it. This applies to landlord policies and standard homeowners policies alike.

Notify your agent before the property becomes vacant — not after a loss. For more on how this new language works, see our main vacant home insurance guide.

Moving to a DP-1 policy before the vacancy period begins is the simplest way to prevent a coverage gap. These policies can be written for short terms and cancelled pro-rata once the property is occupied again.

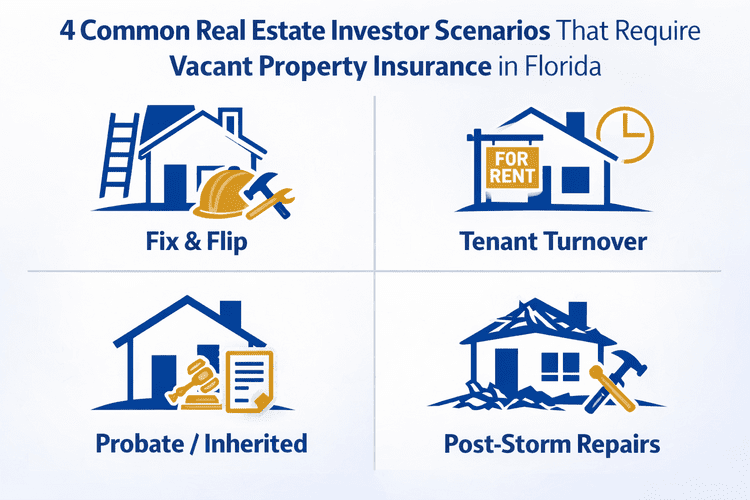

When Does a DP-1 Apply? Common Investor Situations

Understanding how a DP-1 policy applies in practice helps investors plan ahead. Below are real-world situations we see regularly in our agency:

Scenario 1: Fix-and-Flip Renovation

You purchase a distressed property, plan a 90-day renovation, and intend to sell immediately after. No one will live in the home during the project.

A DP-1 policy covers fire, wind, and other named perils during the renovation period. If the project runs long, the policy stays in force. Once the home sells, you cancel and receive a pro-rated refund for unused time.

Scenario 2: Tenant Turnover Gap

Your tenant gives 30 days' notice, moves out, and it takes you 45 days to find a new renter. During that 75-day gap, your landlord policy's vacancy clause may have already kicked in.

A DP-1 bridges the gap. Once the new tenant signs a lease and moves in, your agent transitions the property back to a standard landlord policy.

Scenario 3: Inherited Property in Probate

A family member passes away and you inherit their Florida home. Probate takes six months. The home sits empty with no furniture. This is a textbook vacant property — and a DP-1 is the right coverage until you decide whether to sell, rent, or move in.

Scenario 4: Post-Storm Repair Delays

A hurricane damages your rental property. Your tenant relocates. Repairs take four months due to contractor backlogs and material shortages — a routine timeline in Florida after a major storm.

Your standard landlord policy may not recognize the property as occupied during this period. A DP-1 ensures it stays protected while you wait for repairs to finish.

Have a scenario that doesn't fit neatly into one category? That's normal for investors. Request a quote or call 904-268-3106 and we'll match your situation to the right policy.

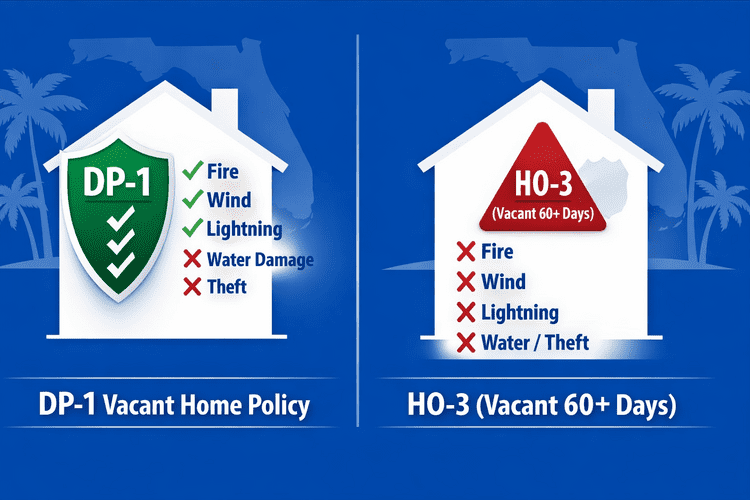

What Does a DP-1 Cover vs. a Landlord Policy vs. a Homeowners Policy?

A DP-1 is a named-peril policy, meaning only the specific events listed in the policy trigger coverage. If the cause of loss isn't named, it isn't covered.

This is more limited than the open-peril coverage on a standard HO-3 homeowners policy or a DP-3 landlord policy — but it provides essential protection for the risks most relevant to a vacant investment property.

The comparison chart below shows how coverage changes depending on the policy type and vacancy status:

| Peril / Feature | DP-1 (Vacant) | DP-3 (Landlord/ occupied property) | HO-3 (If Vacant 60+ Days) |

|---|---|---|---|

| Fire & lightning | ✔ Covered | ✔ Covered | ✘ May be denied* |

| Windstorm & hail | ✔ Covered | ✔ Covered | ✘ May be denied* |

| Smoke damage | ✔ Covered | ✔ Covered | ✘ May be denied* |

| Explosion | ✔ Covered | ✔ Covered | ✘ May be denied* |

| Vandalism | ⚠ By endorsement only | ✔ Covered | ✘ Typically excluded |

| Accidental water damage | ✘ Excluded | ✔ Covered | ✘ May be denied* |

| Theft of personal property | ✘ Excluded | ⚠ Limited | ✘ Typically excluded |

| Liability coverage | ⚠ By endorsement only | ✔ Included | ✘ May be denied* |

| Mold | ✘ Excluded | ⚠ Limited | ✘ May be denied* |

| Wear & tear / maintenance | ✘ Excluded | ✘ Excluded | ✘ Excluded |

| Loss valuation basis | ACV (Replacement Cost available by endorsement) | Replacement Cost | Replacement Cost |

| Pro-rated cancellation | ✔ Yes | ✔ Yes | ✔ Yes |

* Under newer Florida policy language, carriers may deny all perils — not just select ones — if the occupancy change was not reported. See our main vacant home insurance guide for details.

The Water Damage Exclusion: What Every Investor Must Know

This is the exclusion that catches most investors off guard. A DP-1 policy does not cover accidental water damage — no pipe leaks, no plumbing failures, no appliance malfunctions. Because no one is living in the home to catch a leak, carriers remove this coverage entirely from vacant risks.

A burst pipe in a vacant home can run for days before anyone notices, leading to tens of thousands of dollars in damage — none of which would be covered under a DP-1 policy.

Turning off the main water supply before leaving the property vacant is the single most important prevention step an investor can take.

For a full breakdown of how standard homeowners policies handle vacancy, the Insurance Information Institute provides a helpful comparison of dwelling and homeowners policy forms.

Own Vacant Investment Property in Florida?

Talk to an agent who works with landlords, flippers, and real estate investors across the state.

904-268-3106We'll review your situation and walk you through your DP-1 options — no pressure, no obligation.

What Happens If You Don't Tell Your Insurance Company the Property Is Vacant?

This is one of the most common mistakes Florida investors make — and one of the most expensive.

Even if you keep your regular landlord or homeowners policy active and continue paying premiums, a loss that occurs while the property is vacant is almost never covered. Standard policies are written and priced for occupied homes.

Once the property sits empty beyond the carrier's vacancy threshold — typically 30 to 60 days — claims can be denied across the board.

Under the newer vacancy language now appearing in Florida policies, the consequences are even more severe. Many carriers have moved from excluding specific perils (like water and vandalism) to excluding all coverage — including fire, windstorm, and liability — if the insured fails to report an occupancy change.

What This Means in Practice

A tenant moves out, and you don't notify your insurance company. Two months later, a kitchen fire causes $80,000 in damage.

Under traditional vacancy language, fire would likely still be covered. Under the newer all-exclusion language, your carrier can deny the entire claim — leaving you to cover $80,000 out of pocket.

A DP-1 policy for that same property might have cost $1,500 to $3,000 for the year.

Telling the insurance company upfront is always the better path. When you let your agent know the property is vacant, they can switch you to the correct policy type — a DP-1 — which is designed for exactly this situation.

Staying silent doesn't preserve your coverage; it only increases the risk of a denied claim when you need the policy most.

Is Your Property in an LLC? Make Sure the Policy Matches

Many Florida real estate investors hold their properties in an LLC or other legal entity for liability protection and tax purposes. If your property is owned by an LLC, the name on your insurance declarations page must match the LLC name exactly.

If the policy is written in your personal name but the deed is in the LLC's name — or vice versa — your carrier may have grounds to deny a claim. The insured party on the policy must match the legal owner of the property.

Declarations Page Check: Does the Name Match?

Pull your current declarations page and compare the "Named Insured" to the name on the property deed. If your property is held as Smith Investments LLC, the policy should list that entity — not your personal name.

If you've recently transferred a property into an LLC, transferred ownership between entities, or changed the legal name of your LLC, notify your insurance agent immediately. A name mismatch between the policy and the deed can result in a denied claim — even if premiums were paid on time and the policy was in force.

This is especially important when transitioning from a standard homeowners policy to a DP-1 for a vacant property. Your agent should verify the named insured, the property address, and the entity name on the new policy before it's bound.

How Can Investors Protect a Vacant Property Beyond Insurance?

Because DP-1 coverage is more limited than a standard policy, smart prevention is part of the strategy. These steps can reduce your out-of-pocket risk, make the property more attractive to carriers, and help avoid the types of losses that DP-1 policies don't cover — especially water damage.

1. Turn off the water supply

This is the single most important step. Water damage is excluded on DP-1 policies, and leaks are one of the most common and most expensive problems in empty Florida homes.

Shut off the main water supply before leaving the property vacant. If you need to keep water on for contractors, install a leak detection sensor near the water heater and main supply line.

2. Keep curb appeal maintained

An overgrown lawn and dead landscaping signal that no one is checking on the property. Regular lawn care and simple exterior upkeep discourage vandalism and trespassing, and keep the home ready for showings if you're selling.

3. Use lighting timers and keep blinds closed

Basic lighting timers help the home appear occupied during the evening. Closed blinds make it harder for someone to see that the property is empty or spot anything worth taking.

4. Leave internet service active for cameras and sensors

A basic WiFi plan allows you to install a doorbell camera, smart water sensors, and motion detectors. Remote access means you can check in without driving to the property. Some carriers may offer better terms for properties with monitored security systems.

5. Maintain the HVAC system

Even when the property is vacant, keep the heating and air system running at a moderate temperature. In Florida's climate, this controls humidity, reduces mold risk, and keeps the home in better condition for future buyers or tenants.

6. Have someone local check the property regularly

A neighbor, property manager, or trusted contractor walking the property weekly — especially after storms — helps catch small issues before they become large claims. Document each visit with photos for your records.

What Affects DP-1 Pricing for Florida Investment Properties?

DP-1 premiums for vacant investment properties in Florida vary based on several factors. While every property is different, the cost drivers are consistent across the market:

- Property location — coastal and South Florida properties carry higher wind risk and typically cost more than homes in Northeast or Central Florida

- Home condition and age — older homes, deferred maintenance, and outdated electrical, plumbing, or roofing systems increase premiums and may limit carrier options. A 4-point inspection is often required

- Expected length of vacancy — some carriers offer flexible terms, including 6-month policies with pro-rated cancellation

- Security features — alarm systems, cameras, smart water sensors, and deadbolts can improve your risk profile

- Renovation status — properties undergoing active construction may face additional underwriting requirements or higher premiums

- Admitted vs. surplus lines carrier — most vacant properties can be placed with admitted carriers like Tower Hill Insurance or American Integrity Insurance, but properties that don't qualify may require an Excess & Surplus (E&S) lines carrier at higher cost

For context on how standard homeowners insurance is priced in our area, see our latest data in How Much Does Homeowners Insurance Cost in Jacksonville, FL?

To see which carriers are most active in Florida, check our Top 25 Florida Homeowners Insurance Companies ranking.

What We See in Our Book of Business

Most of the vacant investment property policies we manage in Florida are written through admitted carriers on a DP-1 dwelling fire form. Premiums vary widely depending on property specifics, but the most common range we see for investor-owned vacant properties falls between $1,500 and $3,500 per year.

Location, property condition, and carrier selection are the biggest drivers of cost. Since we're an independent insurance agency, we shop across admitted and E&S markets to find the best combination of price and protection for each property.

Checklist: 7 Steps Before Your Investment Property Goes Vacant

Whether you're between tenants, starting a flip, or managing a probate property, complete these steps before the home sits empty:

- 1. Notify your insurance agent — tell them the property will be vacant before the occupancy changes, not after. This is the single most important step to avoid a denied claim.

- 2. Get a DP-1 policy in place — your agent should bind the vacant dwelling fire policy before your standard landlord or homeowners policy's vacancy clause kicks in (typically 30 to 60 days).

- 3. Confirm the named insured matches the deed — if the property is held in an LLC or other entity, the declarations page must list the LLC name, not your personal name.

- 4. Shut off the water supply — water damage is excluded on DP-1 policies and is the most common expensive loss in vacant Florida homes. If contractors need water, install a leak sensor.

- 5. Install cameras and smart sensors — a doorbell camera, water leak detector, and motion sensor connected to WiFi allow you to monitor the property remotely.

- 6. Set up regular property checks — have a neighbor, property manager, or contractor walk the property weekly, especially after storms. Photograph each visit.

- 7. Keep the HVAC running and the lawn maintained — humidity control prevents mold, and curb appeal discourages vandalism and trespassing.

Want this checklist reviewed for your specific property? Call 904-268-3106 or request a quote — we'll walk through each step with you.

Summary: DP-1 Insurance for Florida Real Estate Investors

If your Florida investment property is empty — for any reason, for any length of time — your standard landlord or homeowners policy may not protect you. Many Florida carriers have adopted new policy language that excludes all coverage if you don't report an occupancy change.

A DP-1 dwelling fire policy is the most common way to insure a vacant investment property in Florida. It covers named perils like fire, wind, and lightning, but excludes water damage, mold, and theft.

Based on policies we currently manage, annual premiums for investor-owned vacant properties typically range from $1,500 to $3,500. Admitted carriers like Tower Hill Insurance and American Integrity Insurance write most of these policies, with E&S carriers available for harder-to-place risks.

The most important steps you can take: notify your agent before the property becomes vacant, confirm the named insured on the declarations page matches the property owner or LLC, turn off the water supply, and get the right DP-1 policy in place before a loss occurs.

Need a DP-1 Quote for Your Investment Property?

Share a few details about your vacant property and our Florida team will follow up with options from multiple carriers.

Get a Free QuoteFAQs: Florida Vacant Property Insurance for Investors

Is Florida vacant property insurance the same as a DP-1 policy?

In most cases, yes. The vast majority of vacant home policies in Florida are written on a DP-1 Dwelling Fire Form. This is a named-peril policy designed for vacant, unoccupied, or investor-owned properties. It's different from a standard homeowners or landlord policy, which assumes the home is occupied.

How long can a Florida investment property stay vacant before coverage stops?

Most carriers consider a property vacant after 30 to 60 days without an occupant. Once that limit is reached, your standard landlord or homeowners policy can reduce or deny coverage for many types of losses. Moving the property to a DP-1 keeps coverage in place during the gap.

Does a DP-1 policy cover water damage on a vacant investment property?

No. Accidental water damage — leaks, burst pipes, appliance failures — is excluded on Florida DP-1 policies. Carriers remove this coverage because no one is present to detect a leak before it causes major damage. Shutting off the main water supply is the most important prevention step you can take. For more on the water damage exclusion, see our main guide.

Can I add liability coverage to a vacant Florida investment property policy?

Sometimes. Some carriers allow liability to be added by endorsement to a DP-1 policy, but not all do. Eligibility depends on the age of the home, any updates, and how long the property is expected to remain vacant.

If contractors or prospective buyers will be visiting the property, liability coverage should be addressed before the policy is bound.

Is vandalism covered on a DP-1 policy in Florida?

It depends on the carrier. Some companies include vandalism coverage or allow it to be added by endorsement, while others exclude vandalism entirely on vacant properties. This is one of the areas where working with an experienced independent agent makes a real difference.

Can I cancel a DP-1 policy when the property is no longer vacant?

Yes. Most DP-1 policies in Florida allow pro-rated cancellation — meaning you only pay for the time the policy was in force. Once the property is occupied by a tenant or a buyer takes ownership, your agent can cancel the DP-1 and transition you to the appropriate standard policy.

What if I'm renovating a flip — do I need a DP-1 or a builder's risk policy?

It depends on the scope of the work. A cosmetic renovation — new paint, flooring, cabinets, fixtures — is typically covered under a DP-1 policy.

A major structural renovation — moving walls, adding square footage, new roofing — may require a builder's risk policy instead. If you're doing a light-to-moderate flip, a DP-1 is usually the right call. Your agent can help you determine the right fit.

Do I need a separate DP-1 for each vacant property I own?

Yes. Each vacant property needs its own DP-1 policy. There is no blanket DP-1 that covers multiple locations on a single form. However, an independent agency can often place multiple properties with the same carrier to streamline the process and look for multi-policy pricing.

My property is in an LLC. Does the DP-1 policy need to be in the LLC's name?

Yes. If the property deed is in the name of an LLC or other legal entity, the named insured on the DP-1 policy must match. A mismatch between the policy name and the deed can give the carrier grounds to deny a claim — even if premiums were paid on time. When setting up or renewing a DP-1 policy, confirm with your agent that the named insured, the property address, and the entity name are all correct on the declarations page.

How Do You Get the Right Vacant Property Coverage as an Investor?

Because vacant risks are higher and DP-1 policies vary by carrier, working with an independent insurance agency is essential for investors. Unlike a captive agent who represents one company, an independent agent shops across multiple carriers — both admitted and surplus lines — to find the right fit for your specific property.

Investors often need guidance on details that aren't obvious from a policy quote sheet:

- Availability and terms of vandalism coverage

- Whether liability can be added by endorsement

- How the carrier defines vacancy vs. unoccupancy

- Pricing differences when renovations are in progress

- Maximum vacancy duration the carrier will allow

- Rules that apply during Florida's hurricane season

- Whether the named insured matches the property's LLC or entity name

Your property's location, roof age, updates, and expected length of vacancy all influence eligibility and price. Our team works with carriers across Florida and understands the underwriting rules that affect investment properties between tenants, under renovation, or in estate settlement.

Speak With a Florida Investment Property Specialist

We insure vacant properties for landlords and investors across the state — from Jacksonville to Miami.

904-268-3106Augustyniak Insurance Group | Jacksonville, FL | Independent & Locally Owned