Commercial Auto Insurance

We’ll shop and help you save on your Florida Business insurance.

Commercial Auto Insurance

Last updated:

What Jacksonville Businesses Need to Know About Commercial Auto Coverage

Commercial auto insurance covers vehicles owned or used by a business — including liability for accidents your employees cause, physical damage to your fleet, and coverage gaps that personal auto policies do not address. In Florida, businesses that own, lease, or regularly use vehicles for work are required to carry commercial auto coverage that meets state and contractual liability standards.

It starts with having more than one option. Augustyniak Insurance Group is an independent commercial auto insurance agent in Jacksonville — we do not work for one insurance company.

We compare business auto insurance rates from 10 carriers, including Progressive, Auto-Owners, Travelers, Nationwide, GEICO, Kemper, and National General, to find the right combination of coverage, price, and carrier strength for your fleet.

If you run an established business in Northeast Florida, you are probably asking:

- How much should I expect to pay for commercial auto insurance in Jacksonville?

- Do I actually need commercial auto — or does my personal policy cover business use?

- Which carriers offer the best combination of rate, coverage, and certificate capabilities?

- Am I properly covered if an employee causes a serious accident in a company vehicle?

This guide will walk you through it — simply and clearly.

Want to skip ahead? Get your free commercial auto quote here or call (904) 268-3106.

Whether you manage a contracting crew out of Southside, run a service fleet based near Town Center, or operate work vehicles across Orange Park, Nocatee, and St. Johns County — your business auto insurance is one of the most important financial decisions your company makes each year.

We serve contractors, service companies, delivery operations, professional firms, and food truck operators across Jacksonville and North Florida, including St. Augustine and the Gainesville area.

How Much Does Commercial Auto Insurance Cost in Jacksonville?

Commercial auto insurance costs more than personal auto insurance — and for good reason. Your business vehicles carry more liability exposure, more miles, and more drivers than a personal car. The coverage is broader, the limits are higher, and the risk profile is different.

Based on our book of active commercial auto policies in Jacksonville, most service and trade businesses carrying $1,000,000 in liability pay between $3,000 and $8,000 per vehicle per year. Trucking and heavy vehicle operations typically pay more — often $8,500 to $11,000 or higher per vehicle per year.

A business with three service vans at $1,000,000 combined single limit might pay roughly $9,000 to $15,000 per year for the fleet. A single-vehicle policy for a lighter operation could come around $3,000 to $4,000. It depends on your industry, your vehicles, and your drivers.

The majority of our commercial auto clients carry $1,000,000 in combined single limit liability — because that is what most contracts, general contractors, and commercial leases require. A smaller number carry $300,000 to $500,000 depending on their industry and contract requirements.

Key factors that affect your rate include industry classification, fleet size, vehicle weight, annual mileage, driver records, garaging location, and the limits you select.

At Augustyniak Insurance, we shop your fleet across all 10 carriers in Jacksonville to find the best rate without cutting the coverage your contracts require. Even a modest rate difference per vehicle adds up across a fleet.

As a business owner any opportunity to make things a little easier is always a plus. I am so glad I choose to go with Augustyniak Insurance. Nobody likes dealing with insurance, but Susan and her team made everything hassle free! They have held our policies for the past 4 years and we never had any problems. You feel like you are their only customer. I am happy to say insurance is the last thing from my mind because I know Susan and her team have my whole company covered!!

John — Verified Google Review

Augustyniak Insurance has exceeded my expectations! As another year is about ready to pass, they again have contacted me to do a "sit down" review of my commercial business insurance to make certain I understand my coverage, verify if we need to make any changes and explain any questions I may have. The quality of care they provide to me was top notch!

Cindy — Verified Google Review

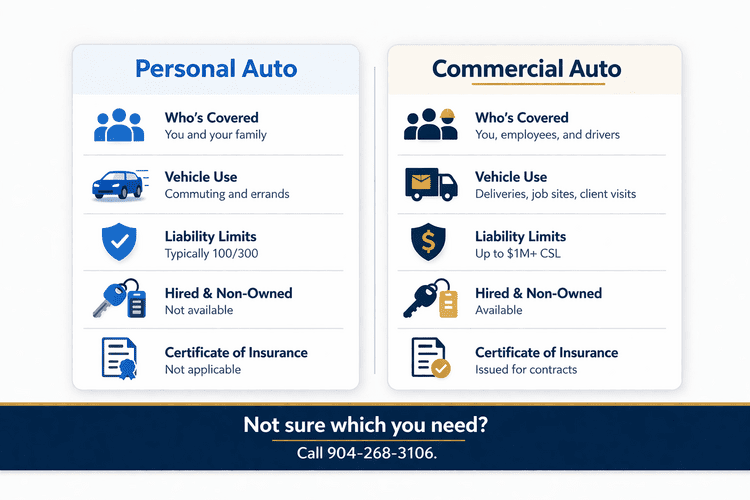

Do You Need Commercial Auto Insurance — or Is Personal Enough?

A personal auto policy covers everyday driving — commuting, errands, and family trips. It does not cover vehicles used for business purposes like hauling materials, making deliveries, transporting clients, or driving between job sites.

If you use a vehicle for business and file a claim, your personal auto carrier can deny the entire claim. That leaves your business exposed to the full cost — medical bills, property damage, legal fees, and lost income — with no coverage behind you.

Commercial auto insurance (sometimes called business auto insurance) is built for business use. It covers your vehicles whether driven by you or an employee, offers higher liability limits, and includes options that personal policies simply do not.

Commercial auto vs. personal auto — the key differences Florida business owners need to know

| Feature | Personal Auto | Commercial Auto |

|---|---|---|

| Business use covered | No — claims may be denied | Yes — built for business |

| Employee drivers | Not covered | Covered under the policy |

| Liability limits | Typically 100/300 or 250/500 | Up to $1M+ CSL |

| Hired & non-owned | Not available | Available |

| Certificate of insurance | Not applicable | Issued for contracts |

Who Needs Commercial Auto Insurance in Jacksonville?

In North Florida and the Jacksonville area, commercial auto insurance is commonly needed for:

- Contractors and trades such as electricians, plumbers, HVAC companies, roofers, painters, and general contractors

- Service businesses with vans, pickups, or work trucks used to visit clients or job sites

- Delivery operations transporting tools, products, food, or supplies

- Businesses with employee drivers using company vehicles during the workday

- Food trucks and mobile businesses that operate on the road or at events

- Real estate investors and property businesses using vehicles for maintenance, management, or renovation work

- Professional firms that want stronger liability protection than a personal auto policy provides

Even if you only use your personal vehicle for occasional business errands — visiting clients, picking up materials, making deposits — your personal auto carrier may deny a claim if they determine you were working at the time of the accident.

Is Your Fleet Properly Protected?

Send us your current policy and we will tell you where you stand — gaps, savings opportunities, and all. No commitment required.

No obligation. No pressure. Just honest answers.What Should a Commercial Auto Policy Include?

A well-built commercial auto policy covers six core areas: liability for injuries and property damage you cause, collision and comprehensive protection for your vehicles, medical payments for your drivers, uninsured motorist coverage, and hired and non-owned auto for rental vehicles and employee-owned cars used for work.

The table below shows three tiers of protection. Most established businesses in Jacksonville carry at least the recommended level. Businesses that sign contracts or work on job sites typically need $1,000,000 in liability.

Commercial auto coverage comparison — what each tier means for your business.

| Coverage Type | Minimum Recommended | Stronger Protection | Maximum Protection |

|---|---|---|---|

| Liability | 100/300 or $500K CSL | $1M CSL | $1M CSL + umbrella |

| Personal Injury Protection | $10,000 (FL required) | $10,000 | $10,000 |

| Uninsured Motorist | $100,000 | $500,000 | $1M stacked |

| Collision | $1,000 deductible | $500 deductible | $500 deductible |

| Comprehensive | $1,000 deductible | $500 deductible | $500 deductible |

| Hired & Non-Owned | Included | Included | Included |

| Commercial Umbrella | Optional | $1M | $2M+ |

CSL = combined single limit. Most contracts in Jacksonville require $1M CSL at minimum. A commercial umbrella extends your liability protection beyond the auto policy limit.

These amounts are far below what any contract or certificate of insurance will require — and far below what a single serious accident can cost. We build every policy to meet real-world contract requirements, not state minimums.

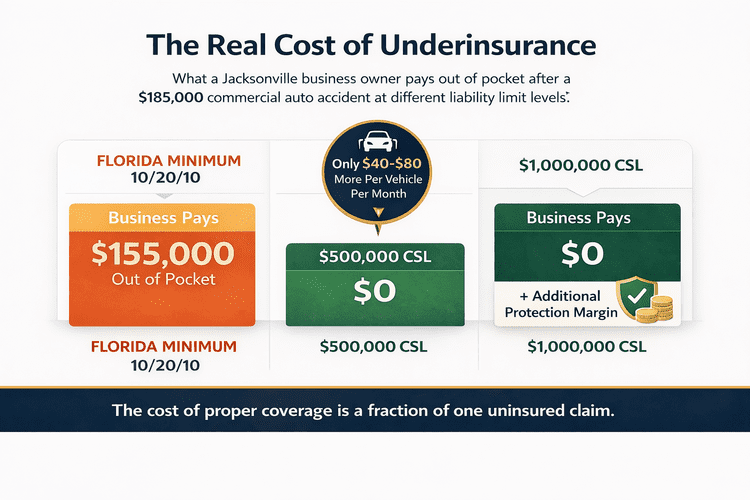

What Happens If Your Business Does Not Have Enough Auto Coverage?

When your policy limits are not high enough to cover a claim, your business is personally liable for everything above those limits.

That means your business assets, equipment, accounts receivable, and even personal assets (depending on your business structure) can be at risk.

According to the Insurance Information Institute, commercial auto claims have increased significantly in both frequency and severity over the past decade.

In a city like Jacksonville — with heavy traffic on I-95, I-295, and J. Turner Butler Boulevard — a single serious accident can exceed $100,000 in combined damages.

A landscaping crew in a company truck rear-ends an SUV during morning traffic. The SUV driver needs surgery. Total medical bills, lost wages, and vehicle repair: $185,000.

Single Limit

Policy covers the full claim

10/20/10 Minimum

Business pays the difference

The cost difference between proper limits and minimum limits is often less than $40 to $80 per vehicle per month. That is a fraction of what one uninsured claim would cost your business — and a fraction of what it costs to lose a contract because your certificate of insurance does not meet requirements.

The real cost of underinsurance — how liability limits protect your business after a serious accident

How Many Vehicles Does Your Business Run?

Whether it is 3 trucks or 15, we compare rates from 10 carriers and find the right coverage for your fleet.

Free quotes. Same-day certificates. No call centers.How Does an Independent Commercial Auto Insurance Agent Compare Carriers?

Not all carriers price the same business the same way. One may be aggressive for contractors. Another may offer better rates for delivery fleets or service companies. That is exactly why working with an independent business auto insurance agent who compares multiple carriers matters.

A Jacksonville HVAC company with 5 service vans, $1,000,000 combined single limit, $1,000 deductible, and clean driver records gets quotes from two carriers through our agency.

(Best Fit)

$336 per vehicle

(Not Optimized)

$445 per vehicle

Same coverage, same vehicles, same drivers — $6,540 saved per year by comparing carriers through an independent agent.

How Do You Get Started?

We Review

Send us your current policy, vehicle schedule, and driver list. We review your coverage, identify gaps, and note where you may be overpaying.

We Compare

We run your fleet through 10 commercial auto carriers and compare rates, coverage terms, and certificate capabilities side by side.

You Choose

We present your best options with a clear recommendation. You pick the one that fits your fleet and budget. No pressure, no games.

How Can Jacksonville Businesses Lower Commercial Auto Premiums?

The best way to lower your commercial auto cost is not to cut coverage — it is to make sure your policy is structured correctly and placed with the right carrier for your business type.

Fleet pricing reduces your per-vehicle cost when you insure multiple vehicles under one policy.

Bundling your commercial auto with general liability, workers' compensation, or commercial property often unlocks multi-policy discounts.

Other strategies include telematics monitoring, defensive driver training, and adjusting deductibles on older vehicles. We cover all nine in detail: How to Save Money on Commercial Auto Insurance in Jacksonville.

Ready to Compare Commercial Auto Rates?

10 carriers. One local agency. Real people who answer the phone.

4.9★ from 2,250+ reviews. Jacksonville's trusted independent agency.How much does commercial auto insurance cost in Jacksonville, FL?

Commercial auto insurance costs more than personal auto because it covers higher liability limits, more drivers, and greater business exposure. Based on our book of business, most service and trade businesses carrying $1,000,000 in liability pay between $3,000 and $8,000 per vehicle per year. Trucking and heavy vehicle operations typically pay more. Your actual rate depends on your industry, fleet size, vehicle types, driver records, and deductibles.

Do I need commercial auto insurance if I use my personal vehicle for business in Florida?

Yes, in most cases. If you use your personal vehicle for deliveries, client visits, hauling equipment, or traveling between job sites, your personal auto policy may deny a claim. A commercial auto policy or a hired and non-owned auto endorsement covers this gap.

What does Florida require for commercial auto insurance?

Florida requires $10,000 in personal injury protection and $10,000 in property damage liability for all vehicles. The financial responsibility law also requires 10/20/10 bodily injury liability after an at-fault accident. Heavier vehicles (over 26,000 pounds) face additional requirements under Florida Statute 627.7415, ranging from $50,000 to $300,000. Most Jacksonville contracts require $1,000,000 in liability — far above the state baseline.

What is hired and non-owned auto coverage and why does my Florida business need it?

Hired and non-owned auto coverage protects your business when you rent a vehicle (hired) or when an employee uses their personal car for any work errand (non-owned). It is inexpensive to add and closes a liability gap that could otherwise cost your business tens of thousands of dollars in a single incident.

What types of businesses need commercial auto insurance in Jacksonville?

Any business that uses vehicles for work — contractors, landscapers, plumbers, electricians, HVAC companies, delivery services, cleaning companies, real estate agents, property managers, and food truck operators. If your vehicle carries tools, materials, or employees to job sites, you should carry a commercial policy.

Can I insure my entire fleet on one business auto insurance policy in Jacksonville?

Yes. Most carriers offer fleet policies covering all your vehicles under one policy with one renewal date and one certificate of insurance. Fleet pricing often reduces the per-vehicle cost compared to insuring each vehicle separately. We help Jacksonville businesses with fleets of 3 to 50 or more vehicles.

What is a certificate of insurance and how fast can I get one in Jacksonville?

A certificate of insurance proves your business has active coverage at specific limits. General contractors, property managers, and commercial landlords typically require one before you can start work or sign a lease.

Our clients have access to a self-service certificate portal for same-day, on-demand issuing of standard certificates. If your contract requires special endorsement language or additional insured wording, our team typically turns those around within 24 hours.

Why should I use a commercial auto insurance agent instead of going direct?

An independent business auto insurance agent compares rates from multiple carriers — not just one company's products. Direct carriers only offer their own pricing, which may not be the best fit for your industry, fleet, or driver profiles. We represent 10 commercial auto companies in Jacksonville and North Florida. There is no extra cost to use an independent agent — the carriers pay us, not you.

When should I review my commercial auto policy in Jacksonville?

At least once a year, and immediately if you purchase or replace a vehicle, hire a new driver, receive a renewal increase, sign a contract requiring higher limits, expand into new service areas, or start using personal vehicles for business errands. An annual review with an independent agent costs nothing and can save thousands.

Can I save money by bundling commercial auto with other business insurance in Jacksonville?

Yes. Bundling commercial auto with general liability, workers' compensation, or commercial property often qualifies your business for a multi-policy discount. Some businesses save 10 to 15 percent or more by packaging their commercial lines through one agency.

What Are Florida's Weight-Based Commercial Auto Liability Requirements?

Florida Statute 627.7415 requires higher liability limits for heavier commercial vehicles. These minimums apply in addition to the standard personal injury protection and property damage liability requirements that cover all Florida vehicles.

The table below shows how Florida's minimum combined liability requirement increases by gross vehicle weight.

| Gross Vehicle Weight | Minimum Combined Liability | Common Examples |

|---|---|---|

| Under 26,000 lbs | 10/20/10 split limit | Vans, pickups, small box trucks |

| 26,000 – 34,999 lbs | $50,000 per occurrence | Medium box trucks, flatbeds |

| 35,000 – 43,999 lbs | $100,000 per occurrence | Large dump trucks, tandem axle |

| 44,000 lbs and above | $300,000 per occurrence | Tractor-trailers, semis |

Source: Florida Statute 627.7415. Vehicles subject to federal FMCSA regulations may require higher limits. Most Jacksonville contracts require $1,000,000 regardless of vehicle weight.

About This Guide

Reviewed by Susan Augustyniak, CIC — Certified Insurance Counselor, Augustyniak Insurance Group. Licensed insurance agent serving Jacksonville and Northeast Florida since 2005.

Augustyniak Insurance Group is an independent insurance agency at 12058 San Jose Blvd, Suite 304, Jacksonville, FL 32223. We represent 80+ insurance carriers across personal, commercial, specialty, and flood lines — including 10 commercial auto companies.

With 2,250+ Google reviews and a 4.9-star average rating, we are recognized by Three Best Rated as one of Jacksonville's top insurance agencies for 12 consecutive years.

This guide was written to help Florida business owners make informed decisions about commercial auto insurance. Cost estimates are based on our analysis of active commercial auto policies in Jacksonville. Regulatory information is sourced from the Florida Department of Highway Safety and Motor Vehicles and the Insurance Information Institute. Coverage recommendations are general guidance — your agent can help tailor a policy to your specific business.

Get a

Get a