Florida's three most problematic wiring types for homeowners insurance are aluminum, cloth, and knob and tube. Here is where each one stands:

- Knob and tube wiring — virtually uninsurable. No standard Florida carrier will write a home with active knob and tube. Complete copper rewire required.

- Cloth wiring — rarely insurable. Most carriers require a complete rewire. A small number may consider the home if the wiring is in documented excellent condition, but this is uncommon.

- Aluminum wiring — only 6 of 17 major Florida carriers accept single-strand aluminum with approved connectors; the other 11 require a full copper rewire. See the full aluminum wiring carrier guide with comparison chart.

All three are flagged during a 4-point inspection and are among the most common reasons for policy declines and non-renewals in Florida.

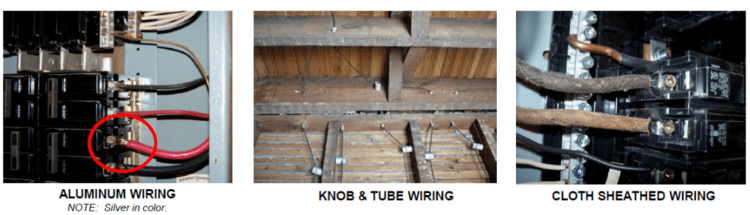

Three types of outdated wiring that can get your Florida home insurance denied: aluminum (left), knob and tube (center), and cloth-sheathed wiring (right).

Outdated wiring is one of the most common reasons Florida homeowners lose their insurance. Not because of a claim. Not because of a missed payment. Because the 4-point inspection revealed wiring that the carrier considers too high a fire risk to insure.

Our agency works with over 80 insurance carriers across Florida, including 26 homeowners insurance companies. We see wiring-related declines and non-renewals every week. This guide is based on what we encounter in actual underwriting, not marketing material.

Below, you will learn what each problematic wiring type is, why insurers care about it, what repairs cost, and what your realistic options are for getting covered. If your home was built before 1980, there is a reasonable chance one of these wiring types is inside the walls. If you are buying an older home, this is something to investigate before you close.

Can You Get Home Insurance in Florida With Cloth Wiring?

It is very difficult to insure a home with active cloth wiring in Florida. Based on our experience placing homeowners policies across the state, most carriers require a complete rewire before they will write a policy. A small number may consider the home if the cloth wiring is in documented excellent condition with no exposed conductors, but this is uncommon and typically requires additional inspection photos and electrician certification.

Cloth-sheathed wiring was the standard in homes built before the 1960s. Unlike modern plastic-insulated wiring, the conductors are wrapped in layers of cloth, rubber, and sometimes tar or paper. At the time it was installed, it was considered safe. Sixty to eighty years later, in Florida's heat and humidity, it is anything but.

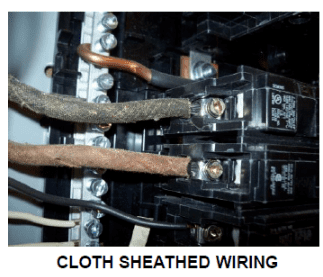

Close-up of cloth-sheathed wiring entering a breaker box. The fabric insulation deteriorates over decades, exposing bare copper underneath.

What Is Cloth Wiring?

Cloth wiring refers to electrical wiring insulated with woven fabric, usually cotton or rayon, sometimes layered over rubber or a tar-like compound. It was the standard residential wiring method from roughly the 1920s through the late 1950s. You will find it in homes built during that period across Jacksonville, St. Augustine, older neighborhoods in Orange Park, and other established Florida communities.

From the outside, cloth wiring looks like fabric-wrapped cable. The insulation may appear brown, black, or gray. In many homes, it has visibly frayed, cracked, or separated from the wire underneath.

Why Is Cloth Wiring a Problem for Insurance?

Insurance companies care about cloth wiring for three specific reasons, all of which increase fire risk:

- The insulation breaks down. Cloth and rubber insulation dries out, cracks, and crumbles over time. Florida's heat accelerates this. Once the insulation fails, live copper wire is exposed inside walls, attics, and junction boxes. Exposed wire near wood framing is how electrical fires start.

- The material itself can burn. The cloth fabric and rubber compounds used for insulation are flammable. Modern plastic-insulated wiring (Romex) is designed to resist ignition. Cloth wiring was not.

- There is no ground wire. Cloth wiring systems were installed before grounding became code. Without a ground conductor, there is no safe path for excess electricity in the event of a fault. This increases the risk of electrical shock and makes it harder to protect modern appliances and electronics.

How Do You Identify Cloth Wiring?

- Look at the wiring entering your breaker panel. If the cables are wrapped in fabric rather than smooth plastic sheathing, you likely have cloth wiring.

- Check accessible wiring in attics, basements, or crawlspaces. Cloth wiring often shows visible fraying, discoloration, or exposed copper.

- Your home's age is the strongest indicator. Homes built before 1960 in Florida are most likely to have cloth wiring.

- A 4-point inspection will identify the wiring type. If you are buying a pre-1960s home, get this done before you close.

What Does It Cost to Fix Cloth Wiring?

Do not attempt any wiring repair yourself. A licensed electrician must do all work, with permits filed and inspections completed.

Cloth wiring does not have a connector remedy like aluminum wiring does. There is no approved method to "retrofit" cloth wiring in place. The only accepted solution for insurance purposes is a complete copper rewire.

- Full copper rewire: $12,000 to $25,000 or more, depending on home size and accessibility

- Permit and inspection fees: $200 to $500 in most Florida counties

- Drywall and paint repair: varies, but rewiring often requires opening walls

It is a significant investment. But a full rewire eliminates the wiring issue with every carrier, reduces your fire risk, and often opens up better homeowners insurance rates because the home's electrical system is no longer a liability.

Can You Get Home Insurance in Florida With Knob and Tube Wiring?

Almost never. Knob and tube wiring is the hardest electrical issue to insure in Florida. Based on our underwriting experience with 26 Florida home insurance companies, no standard carrier will write a home with active knob and tube, including Citizens Property Insurance. A complete copper rewire is the only path to coverage.

If cloth wiring is difficult, knob and tube is the next level. This is the oldest residential wiring system still found in occupied homes. It was the standard from the 1880s through the 1930s. In Florida, you will occasionally find it in historic homes in Springfield, Riverside, Avondale, San Marco, St. Augustine, and other neighborhoods with pre-war housing stock.

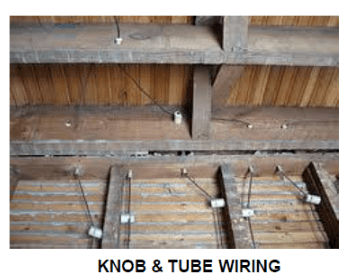

Knob and tube wiring in an attic. The porcelain knobs support the wire along joists, while tubes protect it where it passes through wood framing.

What Is Knob and Tube Wiring?

Knob and tube wiring uses individual insulated conductors run through open air, supported by porcelain "knobs" nailed to framing, and protected by porcelain "tubes" where wires pass through wood studs or joists. There is no cable sheath, no ground wire, and no conduit. The two conductors (hot and neutral) run separately, sometimes several inches apart.

When it was new and properly maintained, knob and tube wiring worked fine for the electrical loads of the early 1900s: a few light fixtures, maybe a radio, and not much else. A century later, the same system is being asked to power air conditioning, refrigerators, computers, and dozens of other devices it was never designed to handle.

Why Is Knob and Tube Wiring Uninsurable?

Insurance companies treat knob and tube as the highest-risk residential wiring type. The reasons are specific and cumulative:

- No grounding. Every modern electrical system includes a ground conductor. Knob and tube does not. Without grounding, a fault in an appliance or fixture has no safe discharge path. This increases shock hazard and fire risk.

- The insulation disintegrates. The original rubber and cloth insulation around the conductors becomes brittle and crumbles with age. In Florida attics, where temperatures can reach 150 degrees, this happens faster. Once the insulation fails, live wire is exposed on open wood framing.

- Circuits are overloaded. Knob and tube was designed for 15-amp circuits powering a few lights. Modern households draw far more. Overloaded circuits generate heat. On wiring that is 80 to 100 years old with failing insulation, that heat becomes a fire hazard.

- Decades of amateur modifications. In many homes, previous owners or unlicensed electricians have spliced new wiring onto old knob and tube, added insulation over exposed conductors (which traps heat), or connected modern appliances to circuits that cannot safely carry the load. Each modification adds risk.

How Do You Identify Knob and Tube Wiring?

- Look in your attic or basement for porcelain knobs nailed to joists and tubes where wire passes through wood.

- The wiring runs in open air, not inside a cable or conduit.

- Two separate wires (hot and neutral) run parallel but apart from each other.

- The insulation, if still present, looks like dark rubber or cloth wrapped around the conductor.

- If your Florida home was built before 1940, check for it. A 4-point inspection will identify it.

What Does It Cost to Fix Knob and Tube Wiring?

Do not attempt any wiring repair yourself. A licensed electrician must do all work.

Like cloth wiring, there is no connector or retrofit option for knob and tube. The only solution is a complete copper rewire.

- Full copper rewire: $12,000 to $25,000 or more

- Older homes with difficult access: costs can exceed $25,000 if walls, ceilings, and attic spaces are hard to reach

- Permit and inspection fees: $200 to $500 in most Florida counties

In historic homes, the rewire is more complex and more expensive because of plaster walls, unusual framing, and the need to preserve original features. If you are buying a historic home in Florida, budget for the full electrical upgrade and factor it into your offer price. A clean electrical system opens up access to all 26 of the home insurance companies we work with, rather than limiting you to the handful that will work with problem wiring.

Can You Get Home Insurance in Florida With Aluminum Wiring?

Yes, if the single-strand aluminum wiring has been properly repaired. Unlike cloth and knob and tube, aluminum wiring has approved connector remedies (COPALUM and AlumiConn) that some Florida carriers will accept. But the carrier you choose matters: based on our underwriting experience with 26 Florida home insurance companies, only 6 of 17 major carriers accept connectors. The rest require a full copper rewire.

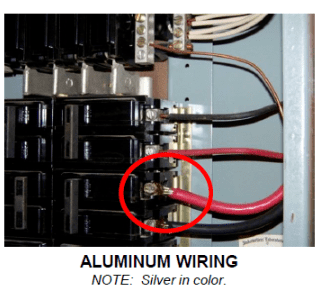

Aluminum wiring is silver in color. Homes built between 1965 and 1975 are most likely to have single-strand aluminum on branch circuits.

We published a separate in-depth guide covering everything about aluminum wiring and Florida home insurance: the difference between single-strand and multi-strand, all three approved repair methods with costs, a carrier-by-carrier comparison chart showing exactly who accepts connectors and who does not, and the documentation you need to pass your 4-point inspection.

Full guide: Can You Insure a Home With Aluminum Wiring in Florida?

Includes a 17-carrier comparison chart, repair cost breakdown, and step-by-step path to coverage.

How Do Florida Insurers Handle Each Wiring Type?

This table summarizes the insurance stance, repair options, and typical costs for all three outdated wiring types, plus modern copper wiring for reference.

| Wiring Type | Era | Insurance Stance | Repair Options | Typical Cost |

|---|---|---|---|---|

| Knob & Tube | 1880s–1930s | Uninsurable | Complete copper rewire only | $12,000–$25,000+ |

| Cloth Wiring | Pre-1960s | Rarely Accepted | Complete copper rewire only | $12,000–$25,000 |

| Aluminum (single-strand) | 1965–1975 | 6 of 17 Carriers | Connectors OR full rewire. See carrier chart | $1,500–$8,000 (connectors) or $12,000–$20,000 (rewire) |

| Modern Copper (Romex) | 1970s–today | Accepted | No repair needed | N/A |

Insurance stance reflects general underwriting trends based on our experience placing policies with these carrier types. Individual carriers may have different requirements depending on the home's full risk profile, location, age, claims history, and other factors. Guidelines are subject to change. Always verify current requirements with your agent before making repair decisions.

Does Your Electrical Panel Matter Too?

Yes. Outdated wiring and outdated panels often go together. If your home has cloth or knob and tube wiring, there is a good chance it also has a panel brand that carriers flag as unacceptable.

Zinsco, Federal Pacific Electric (FPE), Sylvania, and Challenger panels are the most common deal-breakers. All four have documented histories of breakers failing to trip during overloads, which defeats the purpose of having a breaker panel at all. If your home has one of these panels alongside outdated wiring, most carriers will require both to be replaced before they will write a policy.

We cover the full list of problem panels in a separate guide: Electrical Panels That Can Get Your Home Insurance Denied or Cancelled in Florida.

What Should You Do If Your Florida Home Has Outdated Wiring?

1. Find out what you have before it becomes an emergency

Do not wait until your policy is up for renewal or until a carrier sends a non-renewal notice. If your home was built before 1980, schedule a 4-point inspection now. Knowing what is inside the walls gives you time to plan and budget, rather than scrambling after a surprise decline.

2. Get quotes from licensed electricians

Contact at least two or three licensed and insured electrical contractors. Get written quotes that include the scope of work, permit costs, and a timeline. Ask specifically whether they have experience with insurance-related rewiring and whether they provide the documentation carriers require.

3. Make sure the paperwork meets carrier standards

A correctly done rewire with missing documentation can still result in a failed 4-point inspection. Your electrician should provide signed documentation that includes the repair method, permit number, inspection results, and photos of the completed work. Carriers want proof that the work was permitted, inspected, and completed by a licensed professional.

4. Get a clean 4-point inspection after repairs

Once the rewire is complete, schedule a new 4-point inspection that shows the updated electrical system. This is the document your insurance agent will submit to carriers. Without it, the original failed inspection stays on record.

5. Work with an agent who knows which carriers will write the home

Not every carrier evaluates wiring the same way. An independent agent who works with multiple companies can match your home's specific situation to a carrier that will actually approve it. Our agency works with 26 Florida home insurance companies, and carrier appetite shifts constantly. What one company declined last year, another may write today. For a broader picture of who is active in the Florida market, see our breakdown of the 25 largest Florida homeowners insurance companies.

What Are Homes Wired With Today?

Modern homes use copper conductors insulated in plastic sheathing, commonly called Romex or NM-B cable. Unlike every wiring type discussed above, modern copper wiring includes a ground conductor, is rated for today's electrical loads, and is fully acceptable to every Florida insurance carrier.

If your home has been completely rewired with modern copper, the electrical section of your 4-point inspection should be straightforward. The wiring issue is eliminated, and your homeowners insurance carrier options open up significantly.

Has your 4-point inspection flagged outdated wiring?

Our team helps homeowners work through this every day.

We can confirm whether your situation requires a full rewire or a connector remedy, and match you with carriers that will actually consider the home.

Susan Augustyniak, CIC is the owner of Augustyniak Insurance Group, an independent insurance agency based in Jacksonville, Florida. With over 25 years in the insurance industry and a CIC (Certified Insurance Counselor) designation, Susan and her team specialize in helping Florida homeowners navigate coverage challenges including homes with older wiring, problem electrical panels, and other 4-point inspection issues. The agency works with 80+ insurance carriers, including 26 Florida home insurance companies, to find the right coverage match for each home.

The carrier and underwriting information referenced in this article reflects our direct experience as of April 2026. Carrier guidelines change. Individual underwriting decisions depend on the full risk profile of the home, not just the wiring type. Always confirm current guidelines with your agent before making repair decisions based on a specific carrier's requirements.

Frequently Asked Questions About Outdated Wiring and Florida Home Insurance

Is cloth wiring a dealbreaker for home insurance in Florida?

In most cases, yes. Cloth-sheathed wiring is considered a fire hazard because the fabric and rubber insulation breaks down over time, exposing bare conductors. Most Florida insurers require a complete copper rewire before they will write a policy. A small number of carriers may consider a home where the cloth wiring is in documented excellent condition, but this is uncommon and typically requires additional inspection evidence.

Will any Florida insurance company cover a home with knob and tube wiring?

Virtually none. Knob and tube is the highest-risk residential wiring type. It lacks grounding, cannot handle modern electrical loads, and the original rubber insulation disintegrates over time. Even Citizens Property Insurance, Florida's insurer of last resort, will not write a home with active knob and tube wiring. A complete copper rewire is the only path to coverage.

What is the difference between cloth wiring and knob and tube wiring?

Both are outdated, but they are different systems. Knob and tube (1880s to 1930s) uses individual conductors supported by porcelain knobs and tubes, running through open air with no cable sheath. Cloth wiring (pre-1960s) uses conductors wrapped in fabric insulation inside a cable. Both lack grounding. The key difference for insurance is that knob and tube is considered more dangerous because of its age, open-air installation, and vulnerability to amateur modifications.

How much does it cost to rewire a Florida home with outdated wiring?

A complete copper rewire typically costs $12,000 to $25,000 or more, depending on the home's size, age, and accessibility. Older homes with plaster walls and unusual framing tend to be on the higher end. The cost includes the electrical work, permits, inspections, and often some drywall and paint repair where walls need to be opened. This is the only accepted solution for cloth wiring and knob and tube. Aluminum wiring has a less expensive connector option starting around $1,500.

Can I buy a house with knob and tube or cloth wiring and still get insurance?

Yes, but plan for the rewire cost before closing. Many buyers negotiate the rewire into the purchase agreement or request a seller credit. Get the electrical work done, permitted, and inspected before applying for homeowners insurance. You will need a clean 4-point inspection showing the completed rewire, along with the electrician's documentation and permit numbers.

What type of wiring do modern homes use?

Today's homes are wired with copper conductors insulated in plastic (NM-B cable, commonly called Romex). This wiring includes a ground conductor, is rated for modern electrical loads, and is fully acceptable to every Florida insurance carrier. If your home has been completely rewired with modern copper, the electrical section of your 4-point inspection should be clean.

Should I check my electrical panel at the same time?

Yes. Outdated wiring and outdated panels often go hand in hand. Zinsco, Federal Pacific Electric, Sylvania, and Challenger panels are the most common insurance deal-breakers. If your home has one of these panels alongside cloth or knob and tube wiring, most carriers will require both to be replaced. See our full guide: Electrical Panels That Can Get Your Home Insurance Denied or Cancelled in Florida.

Dealing with a wiring issue on your 4-point inspection?

We help Florida homeowners sort through this every day.

Whether it is cloth wiring, knob and tube, aluminum, or a problem panel, our team can walk you through the options and match you with carriers that will actually write the home.

Discussion

There are no comments yet.