Short answer: Florida requires every driver to carry Personal Injury Protection (PIP), which pays 80% of medical bills and 60% of lost wages up to $10,000 per person. MedPay is optional coverage that pays the 20% PIP leaves behind and follows you out of state in any car. Together, they close most of the gaps in a Florida auto policy.

Whether you're driving in Jacksonville, Orlando, Miami, or anywhere across Florida, you know driving in Florida can be stressful. Auto insurance can feel the same way, full of twists and turns.

Florida requires every driver to carry Personal Injury Protection (PIP) on their auto insurance policy, but PIP has strict limits. Many drivers are unaware that these limits could result in thousands of dollars in unpaid medical bills following an accident. That's where Medical Payments coverage (MedPay) on your auto insurance policy comes in.

PIP covers medical bills and lost wages after an accident in Florida, regardless of fault, with a $10,000 per-person limit. MedPay is optional coverage that pays the remaining balance and works out of state.

This article was reviewed by Susan Augustyniak, CIC, owner of Augustyniak Insurance Group in Jacksonville. If you have questions as you read, give our team a call at (904) 268-3106. Let's break down both coverages, how they overlap, and why smart Florida drivers often carry both.

What Is Personal Injury Protection (PIP) on Florida Car Insurance?

Standard or Basic Personal Injury Protection (PIP) in Florida is a required coverage on everyone's Florida car insurance policy. PIP is a no-fault auto insurance coverage that pays 80% of medical expenses and 60% of lost wages after an accident, up to a maximum of $10,000 per person.

PIP is the foundation of Florida's no-fault system, intending to ensure prompt payment of benefits after an accident, regardless of who was at fault. Every driver in the state is required to carry it, making it the cornerstone of auto insurance coverage for Jacksonville and all Florida drivers.

PIP and MedPay are two of the coverages we walk through with every household on our auto insurance in Jacksonville page because they are some of the most commonly misunderstood parts of a Florida auto policy.

Basic PIP Covers:

- 80% of medical bills (ER, ambulance, doctor visits, hospital stays, etc.)

- 60% of lost wages if you can't work after an accident

- $5,000 death benefit

- Maximum payable of $10,000 per person

Per-person limit: PIP pays these benefits for each person covered under your policy, up to $10,000 per injured individual. If three people in your car are injured, each has access to $10,000 of PIP benefits.

Two Florida PIP Rules That Quietly Reduce Your Benefits

Two rules in Florida Statute 627.736 catch a lot of drivers off guard. Most people only learn about them after a crash, which is the worst time to find out.

The 14-Day Rule. You must get initial medical care within 14 days of the accident. Miss that window and your PIP claim can be denied entirely, no matter how serious your injuries turn out to be.

The Emergency Medical Condition (EMC) Rule. Florida PIP can be capped at $2,500 if a qualified medical provider doesn't document an Emergency Medical Condition in your records. This is a common source of insurance disputes after a crash. Ask your doctor about an EMC determination at the first visit.

MedPay doesn't have either of these restrictions. It pays based on your bills, period.

Upgrades to PIP:

You can purchase two types of upgrades to PIP in Florida on your insurance policy, if you ask your agent about them. Typically, MedPay is less expensive for similar (not identical) coverage.

- Extended PIP: Raises PIP coverage from 80% to 100% of medical bills and from 60% to 80% of wages. It's still capped at $10,000 maximum.

- Additional PIP: Increases the limit (for example, $20,000 or more, per person). But the percentages paid are still 80% medical and 60% work loss.

The "Out of State, Out of Your Car = Out of PIP" Rule in Florida

Florida's Personal Injury Protection (PIP) follows you in your own car, but won't apply in rentals out of state or while in friends' cars out of state. It's not a universal safety net, and there is a critical rule that can leave you financially exposed if you don't have supplemental coverage.

The Rule: Your Florida PIP policy will cover you and resident relatives anywhere in the United States or Canada, as long as you are in a vehicle you own that is covered by your Florida policy. (Reminder: This rule applies only to PIP and not other types of coverage on an auto policy.)

- In Florida, your car: ✅ PIP applies.

- In Florida, passenger in another car: ✅ PIP still follows you.

- Out of state, driving your own Florida car: ✅ PIP applies.

- Out of state, rental or friend's car: ❌ No PIP coverage.

Examples:

- Driving your Florida car in South Carolina ✅ PIP covers.

- Riding in a friend's car in Georgia ❌ PIP not covered.

- Rental car in Alabama ❌ No PIP. Not covered.

Not sure if you have a coverage gap?

Send us your declarations page and we will walk through it with you. No pressure, no fee.

What Is MedPay in Florida? How Medical Payments Coverage Fills Gaps

Medical Payments coverage (MedPay) is optional auto insurance in Florida that pays the portion of medical bills PIP doesn't cover after an auto accident. MedPay also follows you out of state, with limits you selected. MedPay is typically affordable coverage. It's especially a great option for people with no health insurance or those with high deductibles or limited coverage.

From Jacksonville commutes on I-95 to Orlando theme park trips or Miami traffic, MedPay closes dangerous coverage gaps. It pays quickly and directly, without deductibles or network restrictions, making it one of the simplest ways to protect yourself and your passengers. While optional, MedPay works hand-in-hand with PIP to ensure you aren't left with thousands in unpaid medical bills.

What MedPay Does Cover:

- Pays the 20% balance PIP leaves behind

- Covers bills above your PIP limit (up to your MedPay limit)

- Works out of state (including rentals and other cars)

- Pays regardless of fault, even if you caused the accident

- Provides a per-person limit (if you and two passengers are injured, each person has their own MedPay limit)

- Pays immediately, no deductibles or network restrictions

- Pays even when your PIP is capped at $2,500 because no EMC was documented

What MedPay Does Not Cover:

- Lost wages

- Replacement services (like childcare or cleaning help)

- Death benefits

Florida PIP vs MedPay: Side-by-Side Comparison

| Feature | Basic PIP | Extended PIP | Additional PIP | MedPay (Medical Payments) |

|---|---|---|---|---|

| Required? | Yes, $10,000 minimum | Optional | Optional | Optional |

| Pays Regardless of Fault? | ✅ Yes | ✅ Yes | ✅ Yes | ✅ Yes |

| Pays First or Second? | First | First | First (higher limit) | Second |

| Medical Bills | 80% up to $10K | 100% up to $10K | 80% up to higher limit | 100% of leftover up to MedPay limit |

| Lost Wages | 60% | 80% | 60% up to higher limit | ❌ |

| Death Benefit | $5,000 | $5,000 | $5,000+ | ❌ |

| Per-Person Limit | ✅ $10,000 per person | ✅ $10,000 per person | ✅ Higher per person | ✅ Limit per person |

| EMC Required for Full Limit? | ✅ Yes ($2,500 cap without EMC) | ✅ Yes | ✅ Yes for basic portion | ❌ No |

| Out-of-State Coverage | Limited (your car only) | Limited | Limited | ✅ Yes |

Real-World Claims Examples: How It Plays Out

Here are real Florida PIP vs MedPay claim examples showing how different coverages work in practice. All examples assume you got medical care within 14 days and an EMC has been documented, so the full $10,000 PIP limit applies.

Scenario 1: $10,000 in Medical Bills (PIP vs MedPay)

Imagine a smaller accident where your medical bills total $10,000 for one person.

Even at this level, the difference between relying on PIP alone and adding MedPay can be dramatic. Here's how your out-of-pocket costs change depending on the type of coverage you purchased:

- Basic PIP only: PIP pays $8,000 (80% of $10,000). You owe $2,000.

- Basic PIP + $5,000 MedPay: PIP pays $8,000 (80% of $10,000). MedPay pays $2,000. You owe $0.

- Extended PIP only: PIP pays $10,000 (100% of $10,000). You owe $0.

- Additional PIP ($20K) + No MedPay: PIP pays $8,000 (80% of $10,000). You owe $2,000.

- Additional PIP ($20K) + $5,000 MedPay: PIP pays $8,000. MedPay pays $2,000. You owe $0.

Scenario 2: $15,000 in Medical Bills

Let's imagine a driver on I-95 in Jacksonville gets into an accident with $15,000 in medical bills. Here's how their coverage would work. Your out-of-pocket costs depend on whether you only carry the state-required PIP, or if you've added MedPay or upgraded your PIP:

- Basic PIP only: PIP pays $10,000. You owe $5,000.

- Basic PIP + $5,000 MedPay: PIP pays $10,000 (max limit). MedPay pays $5,000. You owe $0.

- Extended PIP + $5,000 MedPay: PIP pays $10,000. MedPay pays $5,000. You owe $0.

- Additional PIP ($20K) + No MedPay: PIP pays $12,000 (80% of $15,000). You owe $3,000.

- Additional PIP ($20K) + $5,000 MedPay: PIP pays $12,000 (80% of $15,000). MedPay pays $3,000. You owe $0.

Scenario 3: $50,000 in Medical Bills

Now let's examine a much larger accident that results in $50,000 in medical bills. Here's how your coverage would work. Your out-of-pocket costs depend on whether you only carry the state-required PIP, or if you've added MedPay or upgraded your PIP:

- Basic PIP only: PIP pays $10,000 (max limit $10K). You owe $40,000.

- Basic PIP + $20,000 MedPay: PIP pays $10,000. MedPay pays $20,000. You owe $20,000.

- Extended PIP + $20,000 MedPay: PIP pays $10,000. MedPay pays $20,000. You owe $20,000.

- Additional PIP ($20K) + No MedPay: PIP pays $30,000 (Basic $10K + Additional $20K). You owe $20,000.

- Additional PIP ($20K) + $20,000 MedPay: PIP pays $30,000. MedPay pays $20,000. You owe $0.

Scenario 4: Suing the At-Fault Driver

In Florida, you can step outside of the no-fault system and file a lawsuit against the at-fault driver if your injuries meet the "serious injury threshold," which includes permanent injury, significant and permanent scarring or disfigurement, or significant loss of a bodily function. Given $50,000 in medical bills, it's likely this threshold could be met.

If the at-fault driver has Bodily Injury Liability (BI) insurance, their policy would be a source of funds to pay for your remaining medical bills, lost wages, and pain and suffering. However, unlike many other states, BI coverage is not mandatory for Florida drivers, and many drivers carry low limits in Florida.

- If the at-fault driver has BI insurance, you or your attorney would file a claim with their insurance company for the damages not covered by your PIP and MedPay.

- If the at-fault driver has no BI insurance or low limits, you would need to rely on your own Uninsured/Underinsured Motorist (UM) coverage, if you purchased it.

Important: This option is only available for accidents where you are not at fault. If you cause an accident, you cannot sue yourself or your own insurance company for non-economic damages.

See yourself in one of those scenarios?

Most Florida drivers can add real MedPay coverage for less than they expect. We will quote it across 11 auto insurance companies for you.

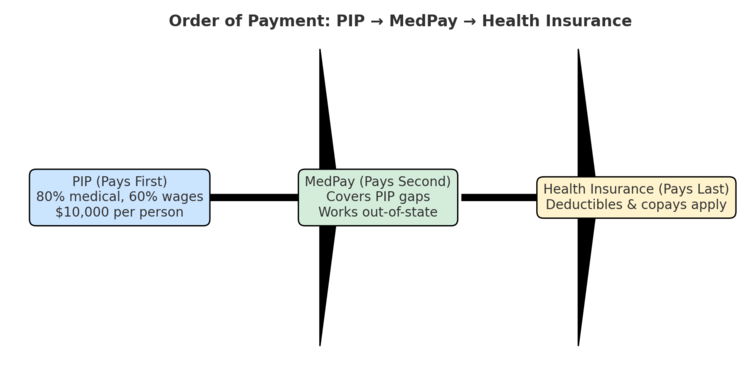

PIP vs MedPay vs Health Insurance in Florida

Florida law makes PIP primary, so your auto policy pays before health insurance.

- PIP pays first (by law, regardless of fault).

- MedPay pays second, covering the gaps.

- Health insurance pays last, often with deductibles and copays.

For families with high-deductible health plans, MedPay can prevent thousands in out-of-pocket costs. It pays your auto-related medical bills before your health plan ever processes a claim, so you don't burn through your health insurance deductible on a car accident.

PIP vs MedPay vs Health Insurance Comparison

| Feature | PIP | MedPay | Health Insurance |

|---|---|---|---|

| Required in Florida? | ✅ Yes | ❌ No | ❌ No |

| Pays Regardless of Fault? | ✅ Yes | ✅ Yes | Silent |

| Order of Payment | Always first | Always second | Pays last |

| Deductibles/Networks? | ❌ None, unless selected | ❌ None | ✅ Yes |

| Covers Lost Wages? | ✅ Yes | ❌ No | ❌ No |

| Per-Person Limit | ✅ $10K+ | ✅ Limit you choose | Depends on the plan |

| Covers Out of State? | Limited | ✅ Yes | ✅ Yes |

Why Florida Drivers Should Care

From daily commutes across Florida to road trips to Georgia or Alabama, coverage gaps are a real risk.

- Example: Imagine you're heading to a Jaguars game with three friends. If everyone gets injured, each person receives their own $10,000 PIP limit plus their MedPay limit. That per-person feature prevents one accident from draining all your benefits.

- PIP alone may not cover you if you're in a rental car out of state.

- Even in Florida, it only pays 80% of medical bills.

- Without an EMC documented in your medical records, PIP can be capped at $2,500 instead of $10,000.

Jacksonville sees more car crashes than any other city in Florida. The Jacksonville Sheriff's Office reported more than 30,000 crashes in Duval County in 2024, and roughly 30% of them were hit-and-runs. I-95, I-295, the Buckman Bridge, Blanding Boulevard, and Atlantic Boulevard are some of the busiest hot spots. MedPay also applies if you're a pedestrian or cyclist hit by a car, which matters in a city that has been ranked among the most dangerous for pedestrians for two decades.

Bottom Line: Adding MedPay to your Florida auto insurance can close these gaps. Get a personalized auto quote, see what auto insurance actually costs in Jacksonville, or call our team at (904) 268-3106.

Ready to review your options?

We shop your coverage across 11 auto insurance companies and walk you through what your policy actually pays. No pressure, no fee, no obligation.

Important Note

This information is provided for general educational purposes only and should not be considered legal or insurance advice. Every situation is different, and coverage can vary based on your policy and carrier.

If you have specific questions about how Personal Injury Protection (PIP) or any other coverage applies to your needs, be sure to review your policy carefully and speak directly with your insurance agent.

If you don't currently have an agent, or would like a second opinion, our team at Augustyniak Insurance Group would be happy to help. We take the time to answer your questions and make sure you have the right protection in place. Call (904) 268-3106.

Frequently Asked Questions (FAQ)

Do PIP and MedPay pay if I caused the accident?

Yes. Both pay regardless of who was at fault.

Are the limits per accident or per person?

They are per person. For example, if three passengers in your car are injured, each gets their own $10,000 PIP limit, plus MedPay if you purchased it.

Do I need MedPay if I already have health insurance?

Yes. MedPay pays immediately with no deductibles or network restrictions, and it covers situations where health insurance may delay or deny claims.

Can I choose MedPay instead of PIP?

No. PIP is required by Florida law. MedPay is optional but highly recommended.

How much MedPay should I buy?

Common limits are $2,000, $5,000, $10,000, or $25,000. Many Florida families choose $5,000 or $10,000 for a strong safety net.

Does PIP cover pedestrians or cyclists in Florida?

Yes. If you're hit while walking or biking in Jacksonville, your own PIP pays first.

Does MedPay cover my health insurance deductible?

Yes. MedPay can reimburse you for deductibles and coinsurance that health insurance leaves behind.

If someone else is at fault, do I still have to file a claim on my own insurance for PIP?

Yes. The first $10,000 of medical bills comes from your own auto policy (your PIP), regardless of who is at fault.

What is the 14-day rule for Florida PIP?

You must receive initial medical care within 14 days of the accident to access PIP benefits. If you wait longer than 14 days, your PIP claim can be denied entirely.

What is an Emergency Medical Condition (EMC) in Florida PIP?

An EMC is a medical condition serious enough that the lack of immediate care could put your health in serious jeopardy. A qualified medical provider must document it in your records. Without an EMC, your PIP medical benefits can be capped at $2,500 instead of the full $10,000.

Susan Augustyniak, CIC

Owner, Augustyniak Insurance Group

Certified Insurance Counselor with more than 25 years in the insurance industry. Before joining Augustyniak Insurance Group, Susan spent nine years at Nationwide Insurance as a commercial underwriter, large loss property claims adjuster, and sales manager. She holds a Florida 2-20 General Lines Agent license and helps Florida families read their auto, home, and business policies. Reviewed and updated May 2026.